A housing boom isn't a win for wealth equality and here's why

I published Billionaire Blindspot in 2024 to draw attention to the poor state of wealth inequality data in Canada and to dispel the intuition Canadians have that we are a much more egalitarian society than our U.S. neighbours. In putting it together, I couldn’t draw on a lot of recent research in the Canadian wealth inequality space because, well, it didn’t exist.

Since then, we’ve witnessed something of a renaissance in the wealth inequality discourse, with great contributions by Alex Hempel, Silas Xuereb and Alex Hemingway, updates from the Office of the Parliamentary Budget Officer (PBO) and an exciting attempt at a new methodology by StatsCan to ascertain how much of our nation’s wealth is held by the very richest families.

These reports are often in conversation with one another, debating methodology and assumptions. I don’t always have much to contribute to those debates; I am mostly just glad to see they’re taking place.

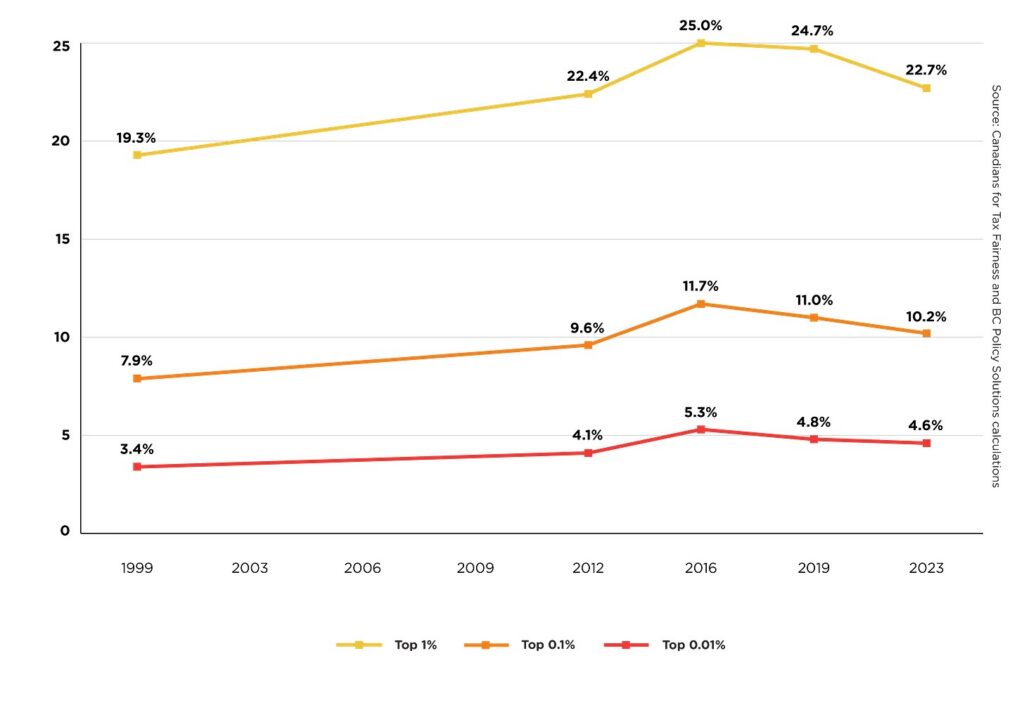

But there’s one finding that’s stuck with me I’ve been wanting to explore in more in depth: the reported decline in wealth concentration of the richest families between 2016-2023, observed by Silas and Alex in The new robber barons: A quarter century of wealth concentration in Canada.

As you can see in their graph, there’s a noticeable dip in the last two data points correlating to 2019 and 2023. On first glance, it looks like the rich got a bit less rich, but that doesn’t really make sense when taken against other trends and measures in our economy. So, what’s going on here? Silas and Alex have a theory, and I think they’re on to something:

“… Another indicator is the trajectory of housing prices. During the pandemic, housing prices increased drastically, inflating wealth for many homeowners. Housing prices began to flatten in 2022 and were actually lower in July 2025 than they were in July 2023, suggesting that the wealth of most households has increased little over this period compared to the rising wealth of billionaires, which is mostly financial wealth,” they write.

To understand what’s actually driving the dip, you need to start with what each group holds. As they point out, typical Canadian families hold the vast majority of their wealth in one asset: their home. The ultra-wealthy hold most of theirs in financial assets like equity in private and public companies. Typically, the financial assets of the wealthy significantly outperform those of ordinary Canadians – which is how we get runaway inequality. During the pandemic years, we witnessed something very unusual instead.

During the pandemic housing boom, national average home prices surged from roughly $504,000 in early 2020 to a record $816,720 in February 2022, according to CREA — a gain of approximately 62% in under two years. Over roughly the same period, Canadian billionaire wealth grew by about 57%, according to Oxfam Canada. For a brief and unusual window, ordinary Canadian homeowners roughly kept pace with — and by some measures outpaced — billionaires!

That role reversal, very rare by any historical measure, is almost certainly what drove the richest families’ share of total wealth temporarily downward. Again, their total wealth didn’t go down, but their proportion of all the wealth in Canada, compared to other groups, did.

Here is where the story gets more complicated. The underlying data for Silas and Alex’s chart comes from Statistics Canada’s Survey of Financial Security (SFS), which runs periodically. According to Statistics Canada’s documentation, the 2019 survey ran September to December under the standard collection window, while the 2023 survey ran April 21 to August 31—an earlier-than-usual window adopted following changes made during the pandemic. This means the height of the housing boom—the surge to $816,720 and subsequent softening—happened entirely in between the two survey periods. No SFS survey captured the peak at all. The dip Silas and Alex observe is therefore real, but it’s measuring the echoes of the boom rather than the boom itself, and it almost certainly understates how dramatically the richest families’ share of total wealth shrank at the actual peak.

There’s a second methodological wrinkle worth flagging that mitigates the significance of the first. The SFS doesn’t use assessed or appraised values for housing. Rather, it asks respondents a single question: “How much would this property sell for today?” StatsCan itself acknowledges that this self-assessment is “subject to a large variance.” Research consistently finds that homeowners overestimate their home values on average, and that price volatility makes accuracy worse, with homeowners specifically tending to overestimate when local prices have recently fallen. The spring and summer of 2023, when the survey was in the field, was exactly that environment: a market that had dropped sharply from its 2022 peak, but with respondents who had spent two years watching neighbours sell for outrageous sums. The anchoring effect of those boom-era prices on self-reported valuations was likely substantial, meaning the 2023 SFS housing wealth figures are probably somewhat overstated relative to where the market had actually settled. The dip in Silas and Alex’s chart may be partly a measurement artifact as much as a real economic phenomenon.

None of this invalidates their finding—the PBO independently confirmed the drop in the richest families’ share of total wealth from 2019 to 2023 is statistically significant but they were using the same SFS data as Silas and Alex did as their baseline. What this does suggest is that the magnitude of the dip, even measured after house prices had already fallen significantly from their 2022 highs, is smaller than the chart implies—and the wealthy are already pulling ahead again. As Silas and Alex themselves note, between July 2023 and July 2025, Canadian billionaire wealth grew 37.2% while total household wealth grew only 9.3%.

Normally, a dip in the richest families’ share of total wealth would be welcome news. But when I look under the hood at what drove this one, I find it hard to celebrate. It was built on a housing boom that temporarily inflated the one asset ordinary Canadians hold. More importantly, the same price surge that temporarily gave ordinary homeowners a larger slice of the pie was a central driver of the housing affordability crisis that has structurally reshaped who can and can’t build wealth in Canada.

For younger Canadians already squeezed by the cost of living, the pandemic housing boom wasn’t a wealth transfer in their direction. It priced them out of the primary vehicle through which most ordinary Canadians accumulate wealth, not to mention a key ingredient most of them seek to feel economically secure and start a family.

A temporary blip in wealth concentration driven by a housing boom that comes at the cost of the next generation’s economic future isn’t progress.

A Conservative case for Community Benefits Agreements?

When a developer builds a new transit line, bridge or hospital, a Community Benefits Agreement (CBA) ensures that the money spent on a large project doesn’t just produce a building, but also provides social and economic advantages to the people living nearby. In Canadian policy circles, CBAs are a file that comes across as relatively left-coded.

I interacted with the file during my time in government and took for granted that the mix of stakeholders involved were relatively progressive, and so were their proposals. Labour unions, local community groups and organizations representing historically marginalized groups all had prominent seats at the table.

And the community benefits they championed reflected that: hiring commitments targeting local workers and underrepresented groups, apprenticeship and training requirements tied to unionized trades and procurement conditions designed to steer contracts toward local and Indigenous-owned businesses. All legitimate goals, but ones that tend to load up a project with conditions before a single shovel hits the ground.

My mental model on the fate of CBAs was simple: a pendulum swinging back and forth. More activity and levers being pulled during NDP/Liberal governments, and a retrenchment or standstill when Conservatives took the helm.

A recent Substack post by Mitch Davidson, Ontario Premier Doug Ford’s former Executive Director of Policy, has me second-guessing that thinking entirely. Could there be an alternate vision for CBAs that aligns with Conservative governments? What if, instead of retrenchment, Conservative governments aggressively pushed forward their own CBA policies with different objectives and criteria? It’s an idea from an unexpected source, but one the traditional CBA stakeholder universe should spend more time thinking about.

Using the backdrop of a specific project, Newfoundland’s Bay du Nord deep-sea offshore oil project, Davidson sketches out a CBA framework that sidesteps what often aggravates the right: additional time delays and cost, unionization requirements and the picking of winners.

Two criteria seem to emerge from this approach. The first is that community benefits can’t seriously impede project delivery, a condition that cuts against some of the more process-heavy CBA frameworks progressives have championed. The second is a preference for long-term economic gains over short-term ones—durable industrial capacity rather than just construction-phase jobs.

In Davidson’s example, the Province of Newfoundland and Labrador opted to abandon previous CBA requirements focused on domestic manufacturing, instead conditioning support on helping the province acquire a floating dry dock facility, something with the potential to bolster the province’s economic fortunes well beyond the life of the project.

That first criteria should give Liberal and NDP wonks pause, because the CBA features they tend to care most about (local hiring commitments, unionization requirements and targeted procurement) are precisely the ones most likely to run afoul of it.

Canadians are losing faith in their governments. They don’t trust that there’s state capacity to deliver ambitious projects on time or on budget—and for good reason. CBAs aren’t the cause of this decline, but it’s difficult to argue with a straight face that poorly designed ones don’t contribute, at least on the margins.

That presents a real opportunity.

With Conservative governments in power across much of the country right now, CBA stakeholders who are willing to engage on these terms have more potential partners than the traditional pendulum model would suggest.

But there’s also a broader lesson here for those of us on the centre-left. Designing CBAs that prioritize delivery isn’t necessarily a concession to the right—it’s how you build the kind of track record that earns the public trust needed to do ambitious things in the first place.

Watch the video: EOTs in Canada - a new succession option for business owners with Jon Shell

What if employees could own the company they work for?

A growing model called employee ownership is gaining attention in Canada, and new research aims to better understand its impact. The Smith School of Business at Queen’s University has launched the Employee Ownership Research Initiative to study how this model works and how it could expand across the country.

In this episode of Moolala: Money Made Simple, Jon Shell, Chair of Social Capital Partners and board member at Employee Ownership Canada, joins Bruce Sellery to explain how employee ownership trusts (EOTs) work and why they could reshape business ownership in Canada.

They discuss:

➡️What employee ownership means and how it works

➡️The purpose of the new Employee Ownership Research Initiative

➡️Current research gaps around employee-owned businesses

➡️Plans to build a national database of employee-owned companies

➡️How employee ownership has evolved in Canada in recent years

This conversation explores how employee ownership could support business succession, strengthen workplaces and create new pathways for shared prosperity.

Speakers

Jon Shell

Chair, Social Capital Partners

Watch the video: The risks and benefits of opening up private markets to everyday investors

The Ontario Securities Commission wants to give retail investors access to private markets. But as SCP Fellow Rachel Wasserman, founder of Wasserman Business Law, tells BNN Bloomberg’s Andrew Bell, when you look closely, it starts to look less like democratization and more like offloading risk onto people with the least power to absorb it.

Private equity is already underperforming S&P index funds over 1, 5 and 10-year periods and PE’s biggest historical champions are quietly reducing their exposure. So, why would regulators suddenly be so eager to open the door for retail investors? This proposal to offer retail investors access to PE stands to benefit the asset managers and intermediaries, with everyday investors bearing the costs and risks. Financial inclusion does not mean broadening access to financial products that sophisticated players are already walking away from.

Speakers

Rachel Wasserman

Founder, Wasserman Business Law

Fellow, Social Capital Partners

Watch the video: Why do Canadians work so hard and get so little?

Low productivity means lower wages and a lower standard of living. Canada does need to boost productivity—but we keep trying the wrong things. Watch SCP CEO Matthew Mendelsohn explain the productivity conversation Canada actually needs to have.

Watch the video: Why would a company sell to its employees?

Canada is facing a $2-trillion business handoff. What if employees owned more of it? Our Director of Policy Dan Skilleter explains why a company would sell to its own employees, how it happens and who stands to benefits. Spoiler alert: employee-owned companies are shown to be 8-12% more productive, share more wealth with their workers, keep businesses Canadian-owned and shore up the resilience of local communities and the broader economy.

How Canada can curb the serial acquisitions quietly reshaping our economy

By Michelle Arnold and Kiran Gill | Part of our Special Series: The Ownership Solution

In recent years, Canadians have watched something change quietly in the economy around them. All of a sudden, there is upselling at the dentist, prices for veterinary care are higher than they used to be and the terms of a gym membership can change out of the blue, with no notice.

In many cases, these threats to day-to-day affordability are the byproduct of what competition experts call serial acquisitions—a pattern of larger firms buying up a series of smaller players to try and corner the market.

The smaller size of these individual transactions means they often fly under the radar of Canada’s Competition Bureau because they’re not big enough to trigger automatic scrutiny.

This makes serial acquisitions notoriously difficult for the government to detect and track, and even more challenging to curb.

The good news is that the Competition Bureau is aware of the negative impact of these quiet deals and is proposing updates to its Merger Enforcement Guidelines, which Social Capital Partners provided formal feedback on. The guideline updates clearly acknowledge the potential negative impacts of serial acquisitions.

This is real progress, reflecting years of advocacy across Canada by an array of organizations, including Social Capital Partners, and a growing recognition that competition policy must address how modern business consolidation actually happens.

But, these new guidelines will also inevitably act as an important test.

Because, while the new guidelines have been in the process of being updated, firms have quietly continued to buy up more companies in sectors across the country.

In 2025 alone, Neighbourly Pharmacy, which bills itself as “Canada’s largest and fastest growing network of community pharmacies,” announced the acquisition of 33 independent Canadian pharmacies. WELL Health expanded its footprint of independent health clinics again, following earlier waves of acquisitions. And U.S.-based AIR Control Concepts entered the Canadian HVAC market to buy up multiple businesses across Ontario and Atlantic Canada.

We can’t say for sure that any of these particular deals will have negative impacts on their customers or communities, but at a time when Canadians are having trouble making ends meet, the evidence shows that consolidations like these come with real risks to both quality and affordability.

Research from the United States has found that consolidation in healthcare services often leads to worse quality of care, while prices for consumers don’t improve—and sometimes even rise. Similar research on the heating and cooling industry shows that, in markets where HVAC competition quietly erodes, prices increase.

The new updated guidelines now explicitly state that a series of acquisitions will be able to be assessed as a whole—often referred to as a “roll-up” of many smaller deals. This is good progress, but this new authority will matter only if it is exercised.

To give the new Merger Enforcement Guidelines teeth, and to stay on top of these quiet consolidations, the Competition Bureau will need to be aggressive with enforcement.

That will mean tracking firms that are actively pursuing acquisition-led growth strategies, using their market-study powers to examine sectors prone to incremental consolidation and improving transparency around merger review results so Canadians can understand how decisions are being made.

The proposed Merger Enforcement Guidelines show clearly that Canada’s competition policymakers understand the problem they are trying to solve.

A fair and competitive economy does not emerge by accident. It requires rules which constrain the consolidation that gives a small number of companies outsized power to set prices, and the tools and resources to monitor behaviour and enforce those rules.

These guidelines can play an important role in keeping prices from quietly creeping up, preventing bigger firms from creating unfair playing fields that hurt small and new businesses and ensuring that Canada’s economy doesn’t concentrate even more wealth and power in the hands of a small number of players. The question now is whether we will be able to follow through.

From Guidelines to Action: Feedback on the proposed Merger Enforcement Guidelines

Background

Social Capital Partners (SCP) is a nonprofit that uses our private-sector experience and public-policy expertise to develop practical policy ideas that help working people build wealth, ownership and economic security.

As we’ve witnessed the increasing consolidation of corporate power in Canada in recent decades, we have concluded that it is impossible to achieve our aims of a fairer, more dynamic, more broadly owned economy without strong competition.

This thinking informed our 2023 submission to the consultation on the review of the Competition Act and our 2025 submission to the consultation on updated Merger Enforcement Guidelines.

Our most recent submission focused on serial acquisitions and the negative impact they can have on our economy. In the time since that submission, serial acquisitions have continued unabated.

For example:

| Pharmacies | In 2025, Neighbourly Pharmacy Inc. announced the acquisition of 33 additional pharmacies across Canada. |

| Primary care clinics | WELL Health acquired 13 primary care clinics in 2024, followed by an additional 9 in 2025, with 34 acquisition opportunities in the pipeline. |

| HVAC | Starting in April 2025, U.S.-based AIR Control Concepts has acquired four HVAC providers, O’Dell HVAC Group, Longhill Energy Products, Airsys Engineering and Rae Mac Agencies. |

We can’t say for sure that any of these particular deals will have negative impacts on their customers or communities, but at a time when Canadians are anxious about making ends meet, the evidence shows they come with real risks to both quality and affordability.

Research from the United States has found that consolidation in healthcare services often leads to worse quality of care, while prices for consumers don’t improve—and sometimes even rise. Similar research on the heating and cooling industry shows that, in markets where HVAC competition quietly erodes, prices increase.

Economic sovereignty is not just about control over essential physical infrastructure, like ports and telecoms. We allow our sovereignty to be chipped away when critical sectors like healthcare, housing repairs and childcare become consolidated in fewer hands – often foreign hands – in ways that make local markets less competitive and create undue obstacles for entrepreneurs to come in and start a business. When private equity (PE) firms systematically consolidate these sectors through serial acquisitions, they gain leverage over critical services, extract wealth and create higher barriers for Canadian entrepreneurs.

In an era in which the U.S. government is using its own companies to advance aggressive foreign policy objectives and openly discussing economic coercion against Canada, allowing further concentration of market power is a strategic vulnerability we cannot afford.

Summary of our feedback on the proposed Merger Enforcement Guidelines

We appreciate the opportunity to provide feedback and believe that the proposed guidelines meaningfully strengthen the clarity and credibility of merger enforcement in ways that are consistent with SCP’s concerns regarding (i) serial acquisitions, (ii) safe harbours and (iii) labour market impacts.

i. Serial acquisitions

SCP recommended that the Bureau more explicitly address serial acquisitions. We are encouraged to see that the Proposed Guidelines clearly articulate the right to examine all or part of a series of acquisitions as a merger, “even if each is not individually notifiable.” We are also pleased to see the proposed guidelines explicitly acknowledge the risks inherent from serial acquisition, by stating “where a firm engages in a series of acquisitions in the same market, each subsequent acquisition may be more likely to result in a substantial lessening or prevention of competition.” This is directionally aligned with SCP’s objective of ensuring that incremental consolidations are

properly assessed in a manner that recognizes their cumulative harm.

ii. Safe harbours

SCP recommended removing or avoiding “safe harbour” framing that could be interpreted as discouraging scrutiny of mergers below certain market share thresholds and are encouraged that the proposed guidelines have moved away from safe-harbour-style signaling.

iii. Labour market impacts

SCP recommended highlighting how labour market impacts should be considered in merger analysis and strongly welcomes the clear inclusion of labour market considerations in the proposed guidelines. This addition appropriately reflects a growing body of policy attention to labour market power as a dimension of competition.

Operationalizing the guidelines

While formalizing the proposed guidelines would be an important step, the real test will be in how the guidelines are operationalized.

We know that the final Merger Enforcement Guidelines will not be a document that is meant to contain details related to operationalization, but we hope that the Bureau will actively and publicly pair their enforcement power with the targeted operational recommendations we outlined in our 2025 submission. Specifically, we recommend that the Bureau:

Identify and more closely track PE firms operating in Canada

Given the outsized role that private equity (PE) firms play in leading anti-competitive efforts to consolidate markets through below threshold acquisitions, the Bureau should allocate dedicated resources to identifying and following the activities of the leading PE firms operating in Canada. This may involve engagement with expert stakeholders, monitoring key data sources, partnering with local governments to monitor mergers regionally, continuing to advocate for the development of a Beneficial Ownership Registry to increase transparency around consolidation patterns and/or introducing legislative tools that compel closed-end funds to report on any acquisitions within Canada.

Issue an open call on the impact of serial acquisitions on consumers and local economic resilience

Seeking feedback from across the country on the impact of roll-ups is an opportunity to access critical information on patterns of transactions that are often opaque and impact a diffuse cross-section of customers. The open call would ideally be done in partnership with local governments and could be specific to sectors like healthcare or be targeted more broadly. Similar efforts are being undertaken in other jurisdictions, with the White House tasking the DOJ, the FTC and the Department of Health and Human Services with issuing a joint Request for Information seeking input on the increasing power and control of the healthcare sector by PE firms. Given the interconnectivity of trade and economic power across the United States and Canada, it would be strategic to follow the United States’ lead and conduct parallel research to inform potential joint action.

Leverage market study powers to obtain information on non-reportable mergers in sectors ripe for serial acquisition

Given the opacity of serial acquisition patterns, the Bureau should take a proactive role in undertaking market studies to understand the state of sectors that are particularly vulnerable to serial acquisition. We suggest a particular emphasis on sectors in the care economy (e.g. long-term care homes, daycares, pharmacies etc.) as these markets are showing clear signs of distress and play a critical role in the health and functioning of our society.

Communicating the guidelines

We also believe that maximizing the effectiveness of the proposed guidelines requires increasing the accessibility of merger information. Canadians are more interested than ever in competition and the impact it has on our economic strength and resiliency. This energy should be leveraged and capitalized on by ensuring that access to pertinent information is available. Specifically, we recommend that the Competition Bureau:

Update the Report of Merger Reviews to be more accessible

SCP welcomes recent changes to the Report of merger reviews, including weekly updates and the inclusion of ongoing reviews. However, examples from jurisdictions like Australia and the European Union, offer valuable models for providing additional information that could improve public transparency regarding merger activity. Specifically, we recommend that the Bureau update the database to include:

- Plain-language summaries of the proposed mergers

- Plain-language summaries of merger decisions

- Relevant decision documentation (not including any sensitive information)

- Links to any additional merger reviews that either party has been involved in

- An option to be notified of new merger reviews as they are announced

Prioritize plain and accessible language in guidance and public information.

Canadians increasingly recognize the importance of competition policy to how people experience the economy. This growing awareness calls for a commitment from the Bureau to ensure that both its guidelines and public information are as accessible as possible. It’s no longer just lawyers and consultants delving into this content, but working Canadians who are concerned with the impact of mergers and acquisitions on their wages, consumer choices and economic well-being. SCP recommends that the Bureau make a concerted effort to prioritize clear, plain-language communication, including providing concrete examples to help Canadians understand the real impacts of economic activities.

Conclusion

The proposed guidelines represent meaningful progress in preserving and protecting competition in Canada. We strongly support their formalization.

However, we believe that the operationalization of these guidelines will be the real test of their impact. Guidance documents shape expectations, but enforcement outcomes shape behaviour. Serial acquirers are sophisticated actors who model regulatory risk into their strategies. If the Bureau does not demonstrate visible capacity to track, analyze and challenge roll-up patterns, market participants will correctly interpret updated guidelines as symbolic rather than substantive.

At a moment when Canada faces unprecedented economic pressure from the United States, allowing continued consolidation of key sectors through unchallenged serial acquisitions weakens our economic resilience and strategic autonomy. The Bureau has the mandate and the opportunity to act.

A youth employment supplement could rebalance Canada’s generational divide | Policy Options

By Kiran Gill and Matthew Mendelsohn | This post originally appeared in Policy Options

The Canadian economy is leaving many young people behind. Young adults today face unemployment rates reminiscent of a recession as well as a housing crisis that leaves many unable to afford necessities. Some 78 per cent of Canadians expect the next generation to be worse off than their parents. Growing wealth inequality has made young people even more pessimistic as they see mounting evidence that the economy is not working for them. They are earning less, saving less and face high barriers to owning assets unless they have help from family.

We also know that Canada’s taxes and benefits are skewed heavily towards serving older people. It is estimated that government spending on those 65-plus is three to four times greater than on those under 45. While Old Age Security (OAS) has become more generous over the last 50 years, government transfers to younger Canadians remain unchanged. At the same time, many seniors pay little or no tax thanks to overly generous tax exclusions, deductions and credits.

Last fall’s budget extended small amounts of funding to various youth employment programs, but the overall numbers don’t lie. The budget includes an increase of $28.3 billion in OAS spending by 2029, but less than $1 billion in new youth employment spending. As our policymakers grapple with how to structure a broad policy response to changes in global economics and geopolitics, we need to address problems with our taxes and benefits as well.

A youth employment supplement (YES) to the Canada Workers Benefit (CWB) would be a creative, scalable, cost-efficient way to motivate young people to get a job, as well as help those who are working but don’t make enough to save and invest. An early version of this model was proposed in a project by graduates Gabriel Blanc, Samuel De Grâce, Kiran Gill and Jacob Kates Rose from the Max Bell School of Public Policy at McGill University.

The Canada Workers Benefit

The CWB offers means-tested tax relief to lower-income working Canadians in the form of a refundable tax credit. All Canadians over 19, except those who are enrolled in post-secondary education or are incarcerated, become eligible for the benefit after the first $3,000 of employment income.

The refundable tax credit increases as income goes up. In 2025, it topped out at $1,633 for individuals and $2,813 for families. The CWB is gradually reduced once adjusted net income reaches a certain threshold. No benefit is received if net earnings are greater than $37,742 for individuals and $49,393 for families. Alberta, Quebec and Nunavut have different negotiated thresholds. Federal legislation allows provinces autonomy in how the CWB is structured.

The CWB, which grew out of a similar benefit introduced in 2007, has had support across the political spectrum and has encouraged people to work and helped reduce poverty (page 29) amongst those who are employed. However, young people are the group most likely to live in poverty and the workers benefit does not do enough for them.

How would a youth employment supplement work?

A youth employment supplement could be created through an amendment to the Income Tax Act that would double CWB payments for single workers between 19 and 29 years old to an additional maximum of $2,000. To ensure the YES were properly targeted, the supplement would be calculated using existing CWB phase-in and clawback rates. Based on 2024 tax data, the average YES benefit for singles would amount to $1,179.

The supplement would not place any administrative burden on recipients. The Canada Revenue Agency would be able to determine eligibility and disburse funds using existing tax data. Based on the current proportion of CWB recipients between the ages of 19 and 29, a YES could benefit close to two million Canadians. And, as the CRA expands automatic filing, even more young workers could seamlessly receive the benefit.

Expected impact

Young adults today face higher hurdles to economic security, home ownership and saving for retirement or emergencies than previous generations. And building assets requires disposable income to invest and save. A 2024 report from Statistics Canada found that 55 per cent of people between the ages of 25 and 44 had difficulty meeting day-to-day expenses. . And a rental survey last summer found that almost half of respondents between 18 and 24 were spending more than 50 per cent of their income on rent, while facing an increasingly insecure job market.

At the same time, young people are carrying growing debt that many are unable to pay off. These debts are increasingly to private credit services that charge extremely high interest rates. A YES would not only help young Canadians meet basic needs, but would also aid them in establishing a viable financial foundation.

Income support programs like this have been shown to improve post-secondary educational outcomes and workforce participation. Research also shows that programs like a YES encourage financial planning and help maintain a stable, consistent standard of living in the face of uncertain income patterns.

Canada is facing significant economic transformation driven by climate change, technology and a rupture in North American and global trading and security. Although the long-term trends are uncertain, we are already seeing reduced hiring, particularly for entry-level professional jobs. Our taxes and benefits need to provide more security and income support to younger workers.

Costing and potential funding sources

In the 2024 tax year, a YES for single adults, defined as those with no spouse or dependents, would cost $2.29 billion. This figure does not include the cost of any changes to the disability supplement (to the CWB) or a YES for couples. These would need to be designed differently and would have additional costs.

By encouraging young adults to work, the added supplement to the CWB would, over time, lead to workforce retention and increased employment rates. And due to its inherent flexibility, it could easily be scaled or altered. Additional income tax revenue from the YES would also offset some of the costs.

New targeted programs, such as a YES, could be funded by reforms to our taxes and benefits. Paul Kershaw, founder of and lead researcher at Generation Squeeze, estimates that modest changes to Old Age Security and age and pension income tax credits would save between $14 billion and $19 billion annually.

An agenda for young adults

Canada is overdue for a broader debate on intergenerational fairness and how our taxes and benefits support — and exclude —different age groups. We continue to live with programs designed by baby boomers to provide security to seniors — even if they are well off. Yet young adults in our country face challenges entering the labour market, securing stable employment and saving to build some measure of economic security in the face of rising costs in almost every sector.

There is almost no government agenda to address this growing disparity. We need policies designed to make the economy work for younger Canadians and to show that Ottawa is responding to their needs. A youth employment supplement could help rebuild financial security and allow younger adults to buy homes, finance education for themselves or their children and save for the future.

Editor’s note: The authors would like to acknowledge Jennifer Robson, Paul Kershaw and Gillian Petit for their insightful comments.

Advocates urge Ottawa to extend ‘no-brainer’ tax incentive for employee ownership | CTV News

By Craig Lord, the Canadian Press | This article first appeared on CTV.ca

It took Peter Deitz eight years to figure out the best way to sell his business. But it wasn’t until the federal government opened up a new option for succession planning that he found the right buyer: his own employees.

Deitz—co-founder of Grantbook, a Toronto-based firm that supports organizations doling out grants to non-profits—said he dreaded the idea of simply selling to an outside buyer who couldn’t see beyond his company’s bottom line.

“I could not foresee a scenario where I would sell the company to a third party that might change that culture or change that special quality within the business,” he said.

Deitz found an alternative he could live with in an employee ownership trust—a vehicle that sees employees of a business get a stake of the firm without having to pay for shares while the owner is paid out over a period of time, typically through the company’s profits.

The federal government first proposed tax changes to facilitate employee ownership trusts in 2023. One of the key measures included in the fall economic statement that year offers a $10-million capital gains tax exemption to owners who sell their companies to their employees through the trust mechanism.

But that exemption was only planned for three years and is set to expire at the end of 2026, unless the federal government moves to extend the measure.

Advocates for employee ownership trusts say letting the tax exemption expire would undercut the model before it’s given a chance to shine. They also argue the vehicle could play a role in defending Canada’s economic sovereignty if Ottawa rallies behind it.Employee Ownership Canada was one of the groups lobbying the federal government to introduce these trusts.

The group’s executive director Justine Janssen said the model is great for employee engagement and for company founders worried about what will happen to their legacy when an outside party takes over and starts looking for efficiencies.

“We’ve had hundreds of businesses reach out and start to understand and contemplate the structure and many are on their way to taking advantage of the trust structure and the capital gains exemption that supports it,” she said.

Janssen said Employee Ownership Canada knows of four trusts established so far in Canada but added another 20 to 30 more could be in the pipeline this year.

Nina Ioussoupova, spokeswoman for the Canada Revenue Agency, said in an email that the CRA does not have “reportable data on the number of employee ownership trusts established to date in Canada.”

She said the “relevant data fields associated with these transactions are not captured in a way that allows for reliable reporting.”

Ioussoupova also declined to say how many company founders have claimed the capital gains tax exemption related to the trusts since it was made available, citing confidentiality provisions in the Income Tax Act.

Employee ownership trusts are a niche option and many businesses are just learning about them now, said Pamela Cross, tax partner at Borden Ladner Gervais LLP.

But if the capital gains exemption is waived, that will only limit their adoption, she said.

That exemption can help to mitigate some of the upfront risks for owners—which are often families trying to cash out from their businesses via the trust.

While employee ownership trusts remove some barriers holding employee groups back from buying out an exiting owner, Cross said financing the transition can be tricky and the model is best suited for businesses with predictable revenue sources.

After a trust is established, exiting owners can retain a minority stake and remain involved in the business but can’t hold a controlling share. Sellers looking to access the capital gains exemption also face a strict test of whether they still effectively control the firm, Cross said.

Some founders may feel letting go of the reins could affect their odds of getting a full payout, she said.

The capital gains tax exemption can also be clawed back if there’s a “disqualifying event” in the years after the sale—essentially, something that stops the business from operating as an employee-owned trust while the seller is still being paid out.

“Certainly there’s been a lot of interest in them,” Cross said. “The concern I have is that the benefits of them are not attractive enough to really make them comparable to a third-party sale, where you can just get paid out on closing and walk away.”

Succession plans are often hammered out over the course of years, not months, and Janssen said the narrow window remaining on the capital gains exemption could limit the number of businesses seriously considering the model.

She said she wants to see the federal government commit to making the tax incentive permanent, or at least offer a defined extension, to give some predictability to owners considering an employee ownership trust.

“We’ve heard many business owners say that that capital gains tax exemption was just enough to make it a no-brainer for them and to feel like they really got fair value and got compensated for that wait time as part of the transaction,” Janssen said.

When asked whether the federal government will extend the expiring exemption, a Department of Finance official told The Canadian Press in a media statement that “while the Government of Canada reviews the tax system on an ongoing basis, it would be inappropriate to speculate on any potential or prospective changes.”

The official noted that the 2025 budget implementation act, which has yet to be passed into law, proposes to extend the exemption to businesses sold to worker co-operatives.

Employee ownership trusts have proven popular in other jurisdictions, including the United Kingdom and the United States—though Cross said the programs in those countries are more generous for founders. In the U.K., for instance, the exemption applies to all capital gains earned from the sale of the business.

Deitz, who earlier this year got the full payout for his employee ownership trust ahead of schedule, did not use the capital gains exemption offered by the government because it’s only available to individual owners, and his stake in Grantbook was through a holding company.

But Deitz also said there should be no cap on the capital gains exemption and that it should apply to small and medium-sized businesses of any ownership structure.

He and Janssen both argue it’s in the federal government’s interest to promote employee-ownership models that keep Canadian companies—and decisions about their intellectual property and the welfare of employees—in Canada.

“This could be the signature project of the Liberal government as a nation-building endeavour to protect the economic sovereignty of Canadian small businesses,” Deitz said.