How to get single family homes out of the hands of investors | Toronto Star

By Matthew Mendelsohn , Mike Moffat and Jon Shell | This post was published in the Toronto Star

Canada needs more rental housing. But it also needs to get existing homes out of the hands of investors and back into the hands of families. The federal government can achieve both simultaneously by fulfilling one of its key campaign promises — with a twist.

Many Canadians are angry about the state of Canada’s housing market, with a recent Abacus poll finding that 56 per cent of Canadians say housing should be a top-3 priority for the federal government. Yet only 28 per cent believe the federal government is on track to meet their housing goals. Many potential homebuyers feel they cannot compete with investors, who have been increasing their share of the resale market.

The federal government is taking some steps to address Canada’s housing crisis. There are programs designed to build new supply, preserve existing affordable supply and reduce demand. But one potentially powerful approach is missing from this suite of programs: incentivizing investors to move their capital to more productive uses…

Budget was missing a Canadian ownership strategy

By Jon Shell | Part of our Special Series: the Ownership Solution | This post first appeared in The Hill Times

The day before the Canadian federal budget was introduced, a Canadian gold mining company called New Gold announced that it would be acquired by American-owned Coeur Mining. This comes only a couple months after the proposed acquisition of one of Canada’s largest miners, Teck Resources, by British-owned Anglo American.

While government approval is still required for these deals to proceed, Ottawa recently signed off on Sunoco’s acquisition of Parkland Corporation, owner of over of 15% of Canada’s gas stations and an important refinery in B.C. That deal provides little or no benefit to the Canadian economy, has already resulted in job losses and turns critical infrastructure over to an American company.

This was the first real test of the newly beefed-up Investment Canada Act, which allows the government to reject acquisitions of companies like Parkland on economic security grounds. The test did not go well.

There was a time when deals like this could be dismissed as just the cut and thrust of global finance in an ever more connected world.

But the federal budget goes to great pains to explain that that those days are over and calls, many times, for “generational investments.”

You know what’s easier than making a generational investment? Not selling the things you already have.

As governments turn protectionist around the world, if Canada stays “open for business,” there’s a significant risk of a repeat of 2006-2007, when foreign investors scooped up major Canadian companies like Inco, Falconbridge, Noranda, Stelco and ATI.

The impact of the loss of head offices, research jobs and control over Canadian resources is still being felt today.

Recently, the current American owner of Stelco, one of Hamilton, Ontario’s major employers, came out in favour of the American tariffs on steel that are harming his own Canadian employees, raising the ire of Ontario Premier Doug Ford.

While the recent budget used the word “sovereign” 81 times, it did not define a clear strategy to build and maintain Canadian ownership of our assets.

When combined with its focus on attracting private capital, there’s a real danger that the federal government will enable a sell-off of Canadian companies to foreign investors. It’s even possible that this sell-off would be considered a “win” for the strategy, as it could be characterized as an investment in Canada.

This would be a mistake.

There is a significant difference between investing in building and investing in buying.

Building leads to new assets, like the Kitimat LNG terminal in B.C., funded in large part by foreign capital. Buying often leads to a loss of head office jobs, innovation capacity and sovereignty.

With the government signaling a willingness to sell Canada’s airports and ports in this budget, bringing back memories of Ontario’s disastrous sale of Highway 407 to a Spanish company, it’s dangerous to proceed without clearly defining what kind of foreign investment we’d accept.

The mistake could easily be corrected with four concrete steps:

First, the budget sets out to “build, protect and empower Canada.” A Canadian ownership strategy fits cleanly in the “protect” column. It could define Canadian ownership more narrowly and ensure that programs like the Scientific Research and Experimental Development tax incentive do not benefit foreign-owned companies.

Secondly, it could reject the proposed acquisitions of Canadian mining companies, making it clear Canadian ownership is a priority.

Thirdly, it could prioritize ownership structures that enhance sovereignty, like employee and community ownership.

Finally, it could tie all these together with other pro-Canadian measures in the budget, like the Critical Minerals Sovereign Fund into a strong and important narrative that Canadians would support.

When a Canadian company is sold, it can be decades before the impact is fully understood.

At the time of its sale to AMD in 2006, ATI, based in Mississauga, shared the global market for graphics chips equally with U.S.-based Nvidia. Today, Nvidia is the leading global supplier of chips that power AI, employes 36,000 people and is worth $5 trillion USD.

AMD bought ATI for $5.4 billion USD and employs fewer Canadians today than in 2006, despite promising to keep a major research centre in Canada.

The U.S. is leveraging Nvidia’s success in their trade war with China. Imagine if that power resided in Canada instead?

If we really want to build a Canada that is “confident, secure and resilient,” we can’t afford to repeat the mistakes of the past.

Sovereignty requires ownership. It’s clear that China and Trump’s America understand that. It’s time for the Canadian government to prove that Canada understands it too.

What the new World Inequality Report tells us, and why it matters for Canada

Economic growth is often treated as a shorthand for progress. As the old story goes, if our Gross Domestic Product (GDP) goes up, then we’re all better off.

But the latest World Inequality Report offers another sobering reminder that who benefits from economic growth matters just as much as how much the economy has grown. And the economic order keeps tilting further and further towards serving a tiny, ultra-wealthy minority.

This is why the World Inequality Database (WID) and this flagship 2026 report matter so much. Launched in 2018, the global effort brings together more than 200 researchers to track income and wealth inequality over time, building a shared global infrastructure to understand—and sometimes even expose—trends that were previously hidden or fragmented.

Canada is a part of this global network of experts, which is vital—because, as we have said in our own 2024 Billionaire Blindspot report, you can’t fix what you can’t see.

The most important new finding is that today’s inequality story is not primarily about the richest 10%, or even the richest 1%. It’s about what’s happening at the very top of the wealth distribution.

Globally, the richest 0.001%—think of them as roughly 60,000 people, or the world’s billionaires, or how many people can fit in a football stadium—have dramatically increased their share of total wealth.

In 1995, this group held about 3.8% of global wealth, but by 2025, that share had climbed to 6.1%. Over the same period, their personal wealth also grew at annual rates between 2% and 8.5%, far outpacing the bottom half of the population, whose wealth grew at just 2% to 4% per year.

When policy debates focus on “the rich” as a broad category, they miss the fact that most of the action is concentrated among a very small number of families (and tech bros) at the extreme top. Looking only at the top 10% or top 1% risks obscuring the true scale—and drivers—of wealth concentration.

Why does this matter? The evidence is overwhelming that growth that produces extreme inequality leads to less resilient, less healthy and less prosperous societies. And economic inequality drives prices and asset values out of reach, depriving ordinary working people from access to goods and services.

It also entrenches power.

“The result is a world in which a tiny minority commands unprecedented financial power, while billions remain excluded from even basic economic stability,” the authors, led by Ricardo Gómez-Carrera of the Paris School of Economics, write.

In Canada, too, although Canada’s GDP keeps going up, wealth gains have been concentrated at the very top. Many Canadian households are struggling to afford food and housing.

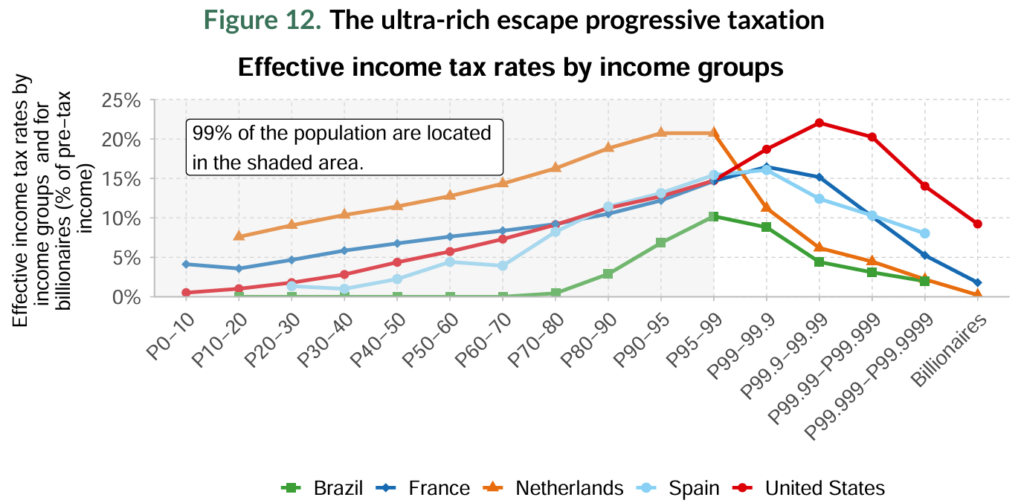

As our colleagues at the Canadian Tax Observatory have also pointed out, one key factor is taxation—or more precisely, who governments are willing or able to tax. International data in the report show a striking pattern: at the very highest income levels, effective tax rates actually decline (see Figure 12 from the report, below). In other words, the ultra-rich often pay lower effective tax rates than those who are merely “rich,” and in some cases, even lower than middle-income earners.

Canada-specific data at this level are notoriously hard to come by, but SCP’s own research suggests a similar dynamic. The wealthiest Canadians increasingly derive their income from capital gains, rather than wages, which are taxed at a lower rate. Our tax system, while containing many progressive elements, actually exacerbates the problem of growing wealth inequality. Because of tax breaks for capital gains and dividends, tax rates on income derived from wealth are lower than those on income derived from working. And that’s before even considering the kinds of sophisticated tax-planning and wealth sheltering strategies that only the wealthy tend to have access to.

The report ranks countries based on the number of data sources they use to measure wealth inequality and Canada sits in the middle of the pack—behind the U.S. and much of Western Europe in terms of transparency and data coverage.

Without high-quality data, policymakers are left debating inequality in the dark. The one-page country profiles in the World Inequality Report are short, but the Canadian profile is revealing. The report’s estimates show greater wealth concentration than the most recent Canadian Parliamentary Budget Officer (PBO) figures based on “rich lists.” For example, the report estimates that the top 1% in Canada hold about 29.3% of total wealth, compared to 23.8% in the PBO’s analysis.

Momentum is building in Canada for better wealth data. Statistics Canada recently released its first serious attempt at improving measurement of wealth at the top—something SCP has long called for. It’s a promising step toward shedding light on Canada’s billionaire blindspot.

The deeper challenge is policy. As Canada faces an unprecedented economic assault from the south, there is a risk that the policy instruments we deploy to encourage growth will exacerbate inequality. We do not want to encourage growth that sees all the returns go to those who already have extreme wealth. We need to tackle the structural dysfunction within the economy today that sees gains and redistribution flow almost entirely upward.

That means better ways for families and communities to build assets—like affordable housing, business ownership, retirement security and emergency savings—alongside tax and regulatory reforms that ensure fair taxation of the ultra-wealthy.

The World Inequality Report is clear: wealth inequality is not inevitable. It is the result of choices.

And when the richest 10% of the world’s population owns 75% of wealth and the bottom half just 2%, it’s time we choose something different.

Ontario wakes up to the succession tsunami

By Dan Skilleter | Part of our Special Series: the Ownership Solution

While it never cracks their Top-10 lists of policy asks, small-business groups and local chambers of commerce have for years been beating the drum of concern over the impending retirement of a massive cohort of baby-boomer business owners. The CFIB’s seminal 2023 report, Succession Tsunami, looms large in the discourse, with its eye-popping statistics of 76% of owners planning to exit over the next decade, with only 10% having a succession plan.

However (with the notable exception of Quebec), it’s a topic that governments across Canada have barely lifted a finger on. Which makes Ontario’s recent public foray into this policy space worth paying attention to.

Last week, Ontario unveiled their plan to implement Budget 2024’s commitment to invest $1.9 million over three years to establish a business succession planning hub. Its newly launched website, SuccessionOntario.ca, helps owners understand their options and funnels them towards a local Small Business Enterprise Centre (SBEC) for tailored advice and services.

They’ve decided to target so-called “micro businesses” and, from what I understand, a lot of the money is going into training and resources for SBEC staff across the province. The average business owner they’re targeting is of a generation that prefers in-person meetings to internet modules—so this approach makes sense.

A couple of interesting things.

First, it was a welcome surprise to see the succession hub’s focus on employee ownership. Featured prominently as the second ‘exit option’ for owners, it’s a strong sign that Canada’s relatively new Employee Ownership Trust (EOT) is breaking through. The EOT is a policy near and dear to my heart, and one I’ve been helping to support the policy design and advocacy of for years. Seeing Ontario recommend it to owners casually alongside options like intergenerational transfer is a sign that it’s becoming mainstream. [1]

Second, the government has adopted an all-too-familiar approach to its problem definition. They view the succession issue as too many business owners without the time, information or know-how to begin their exit planning before it’s too late. Success looks like owners engaging in succession planning early and finding a buyer willing to pay market rate. Any buyer will do.

While important, their framing is single-mindedly focused on the retiring business owner. It overlooks the outcomes for everyone else after the dust has settled. There’s a wide array of buyers out there, each with different implications for the future of the company, its workers and the local community where the company’s located. A foreign private equity firm is a very different new owner than a young entrepreneur, or the employees of the company itself.

The government’s policy lens should be expanded and include a broader commitment to the ongoing resilience, growth and sovereignty of the economy—its slogan is Protect Ontario, after all.

The amount of money Ontario has put into this so far is miniscule, but I take it as a positive signal that succession has finally reached the coveted podium of ‘policy file’ within the bureaucracy.

In 2026, expect Social Capital Partners to spend a lot more of its time working with governments like Ontario on building out the research and ideas to ensure Canada has the right sort of policy infrastructure to withstand the oncoming tsunami.

[1] For those of you who aren’t familiar, the EOT is new federal policy that is tailor-made to help business owners to sell their companies to their employees. For an overview, this is a good start.

Mapping the economic centre-left

There’s an experience I have on a more regular basis than I’d like to admit. Maybe you’ve had it, too.

I’ll read a few economic blogs or listen to podcasts discussing a major trend or issue with the economy, and I’ll be nodding along in agreement with several of them, only to be hit by the realization afterwards that they were espousing some pretty different centre-left (maybe even contradictory) premises.

This has especially been the case in the American blogosphere, which is large and well-funded enough to have seen a pretty wide array of voices and ideological camps emerge within the centre-left tent. So big, in fact, that there’s a sub-genre of inter-blog conflict dedicated to people named Matt. (1)

One piece will insist that the real problem with the economy is financialization, another will argue that what really matters is building more. A third might claim the real issue is that the state no longer has the capacity to do big things. Then someone else will say that the market rules themselves are rigged, so none of the rest matters until we fix that.

They all make compelling cases, at least in part.

Over the years, I’ve found it useful to categorize these different centre-left ideological camps in my head.

They’re not mutually exclusive, and most people probably identify with a few at once. But each has its own story about what’s wrong with the economy and how they’d prioritize dealing with it.

Here’s how I’ve come to think about them:

1. Anti-Extraction

The economy rewards financial engineering and short-term profit over productive investment. Corporate incentives push firms to strip assets, buy back stock and chase quarterly returns rather than build.

2. Pre-Distribution

The “rules of the game” are tilted. Labour laws, competition policy and procurement all favour capital and incumbents. The problem isn’t just inequality; it’s that markets are designed to produce it.

3. Market Socialism

Some goods and services (think healthcare, housing, energy or even grocery) just don’t work well when run for profit. Private ownership in these sectors tends toward fragility and exploitation.

4. Anti-Monopoly

Big firms have grown too dominant, smothering competition and innovation. Whether it’s tech, grocery or telecom, concentrated market power harms consumers and suppliers alike.

5. Community / Localism

Wealth and ownership have become too detached from place. External investors extract profits from communities, leaving them hollowed out.

6. Mission-Oriented

Markets are good at incremental innovation, but bad at solving big public challenges. The state needs to set national missions (decarbonization, housing, biotech) and mobilize private effort around them.

7. Abundance

Our biggest problem isn’t greed or inequality, it’s scarcity—especially of housing, infrastructure and clean energy. We’ve made it too hard to build, thanks to endless permitting and restrictive zoning.

8. Redistribution First

Inequality is baked into capitalism. No matter how we tweak the rules, markets will generate unequal outcomes. That’s fine, but we need strong taxes and transfers to rebalance things after the fact.

The Camps

Camp |

Core Problem with Economy |

Default Policy Instinct |

Who’s the bad guy? |

Key Detractors on Left |

| Anti-Extraction | Corporate incentives and capital markets reward short-term extraction of value (financialization, asset-stripping) rather than long-term investment and value creation. | Reform corporate governance, finance and incentive structures to reward productive, sustainable business models. | Financial engineers — Wall Street, Bay Street, private equity, hedge funds, shareholder activists — who extract short-term profits rather than build productive enterprises. They gut firms, communities and long-term prosperity to feed financial returns. | Abundance advocates who see this as slowing necessary build-out; some mission-oriented strategists. |

| Pre-Distribution | The “rules of the game” in markets are tilted toward capital over labour, incumbents over new entrants and concentrated wealth. | Rewrite market rules to give workers and smaller players more power and share of returns (labour law, competition, procurement, ownership diversification, social wages, universal childcare and transit). | Rigged market rules that privilege employers and capital over workers and communities. The villains are less individuals than the system—weak labour laws, tilted corporate governance, procurement rules that reward low-road business models. | Abundance advocates wary of heavy market rules (‘everything bagel’ liberalism) which can stifle building. |

| Market Socialism | In certain essential sectors, private ownership inherently produces affordability and resilience failures—even with strong regulation. | Sovereign wealth fund, public banks, Crown corporations. | Private profiteers in essential goods/services (for-profit LTC chains, telecom monopolies). Things too essential to be left to profit-seeking should be in public/communal hands, but rent-seekers keep them privatized. | Mission-oriented who want private sector partnerships; pre-distribution/anti-monopoly/anti-extraction who would say that a better way to solve problems is to heavily regulate and change the rules. |

| Anti-Monopoly | Excessive market concentration lets dominant firms exploit consumers, workers and suppliers while stifling innovation. | Break up dominant firms, block anti-competitive mergers and regulate powerful players to restore competition. | Dominant corporations and monopolists (Big Tech, Big Grocery, Big Banks) who squash competition, exploit consumers and bully workers. Concentrated private power is incompatible with democracy and free markets. | Redistributionists who say it’s too slow/indirect; some mission-oriented actors who worry about hindering scale and creating national champions for a strategic purpose. |

| Community/Local | Wealth and ownership are too concentrated in extractive firms and external investors, leaving communities dependent, disempowered and vulnerable. Local economies often “leak” value rather than building lasting prosperity for residents. | Redesign economic institutions so that ownership, control and investment are rooted in communities. The goal is to “lock in” wealth locally and ensure it circulates broadly. | Extractive corporations, absentee landlords, private equity firms and external investors who strip value from communities and displace local economic control. | Some redistribution-first advocates who argue that CWB is too slow and incremental compared to direct taxation/transfer. Certain post-growth advocates may see local economic development as still reproducing growth logics. Some abundance/mission-oriented thinkers may see CWB as parochial or insufficiently focused on national-scale innovation and scaling. |

| Mission-Oriented | Markets alone underinvest in solving big societal challenges and fail to align innovation with public needs. | Use active state leadership—investment, procurement, R&D, conditionalities—to mobilize private sector toward national missions. | Short-sighted markets and timid governments that fail to rise to big challenges (climate, health, innovation). Incumbents defend the status quo and the real villain is a lack of ambition and direction. | Anti-monopolists who fear entrenching “national champions.” Redistribution-first proponents who think this approach doesn’t solve the fundamental economic problems. |

| Abundance | Chronic undersupply and bottlenecks in key goods/services drive up costs and limit opportunity. | Remove barriers to production and speed up approvals/builds to rapidly scale supply in housing, energy, infrastructure, etc. | Bottleneck creators—NIMBYs, slow regulators, legacy incumbents—who block supply and keep things scarce (housing, energy, infrastructure). Red tape, restrictive zoning and entrenched veto players drive up costs for everyone. | Redistributionists who see it as neglecting equity; anti-extractionists who fear quality/sustainability trade-offs. |

| Redistribution First | Markets naturally generate large inequalities in income and wealth; these imbalances undermine fairness, opportunity and social cohesion. | Use the tax-and-transfer system to redistribute income/wealth and fund universal public services after the fact. | The super-rich who hoard wealth and dodge taxes. They’re not playing fair, they can easily afford to pay more and they corrupt democracy by resisting progressive taxation. | Anti-monopolists, abundance advocates who see this as ignoring supply constraints. Pre-distribution/anti-extraction/anti-monopolists who disagree on tackling problems upstream instead of downstream re: theory of change. |

When the people and organizations I respect in Canada or the U.S. disagree on how to best respond to the policy issue du jour, it’s usually because they’re prioritizing what the root economic problem is differently. Sometimes the diagnoses overlap, sometimes they clash. But each perspective offers a distinct set of tools.

And while clashes between these camps are usually entirely avoidable (preferably so), I find them fascinating when they happen: Abundance advocates finding anti-monopoly reformers to be too focused on process, not outcomes. Redistributionists thinking abundance advocates underestimate power and inequality. Mission-oriented advocates worrying that localists are too small-ball. And so on.

These frictions are what make this ecosystem intellectually rich. But in practice, progress often comes from borrowing across camps, creating coalitions and finding the best lens for the problem at hand.

I’ve shared this breakdown with a few wonk friends who found it interesting, so thought it would be worth publishing more broadly.

(1) Yglesias, Stoller, and Bruenig

How intergenerational inequality threatens trust in democracy | Policy Options

By Jean-François Daoust, Liam O'Toole and Jacob Robbins-Kanter | This post originally appeared in Policy Options

The well-documented cost-of-living crisis plaguing young Canadians has triggered deep anxiety about their future – whether they can build stable careers, afford homes or one day raise families.

This is not only an economic problem. It’s a political one. As intergenerational inequality persists and deepens, Canada risks experiencing an even sharper decline in trust in its democratic institutions than what already exists.

To combat this, our political leaders must be willing to make difficult tradeoffs that rebalance priorities toward the young. That means rethinking tax incentives, addressing budget deficits that will fall on future generations and ensuring public spending supports those still trying to build their lives, not just those comfortably established – the group that is the focus of most politicians today.

The young face widespread problems

Home ownership, which has been a cornerstone of middle-class security for decades, is now one of the clearest markers of generational division. For most young Canadians, even saving for a down payment has become very challenging.

As existing homeowners’ properties have ballooned in value at the same time, the housing market has become a mechanism of (unequal) wealth transfer from the young to the old – reinforced by governments that are reluctant to confront politically powerful older homeowners.

The broader economic picture for younger Canadians also offers little hope. Wages have stagnated while costs have soared. Young Canadians are more educated than any previous generation, yet many work at precarious jobs with low pay, unstable hours and few benefits. Student debt and unaffordable child care make it harder to build savings or start families. Indeed, many people are reluctant to have the number of children they would like.

Previous beliefs that education and effort can lead to upward mobility no longer ring true. Instead, young Canadians face economic realities that demand more but give back less.

Politicians listen to older voters, not the young

This economic frustration runs hand-in-hand with political alienation. Older Canadians vote in greater percentages, contribute more to political campaigns and therefore wield disproportionate influence. Politicians cater to their interests and make sure to focus on the issues most important to older citizens.

Younger voters, facing economic instability and disillusionment, are increasingly disengaged from the political process, which only perpetuates their exclusion. This negative feedback loop erodes faith in democracy itself because young Canadians increasingly view politics as unresponsive to their needs.

The effects of this generational divide are already visible in Canada’s political landscape. Young Canadians vote at significantly lower rates than their older counterparts. In the 2021 federal election, only about 46 per cent of eligible voters aged 18 to 24 cast a ballot, compared with nearly 75 per cent of those 65 and older.

Surveys also show that younger Canadians express less confidence in elected officials, political parties and government institutions than any other age group. Many believe that no party truly represents their interests and that the political system is stacked in favour of homeowners and retirees.

It’s time to act

For younger generations, other forms of civic engagement, such as volunteering or signing petitions, may soon see further declines, according to a 2022 federal government report. This erosion of political participation is not apathy born of ignorance, but frustration born of exclusion. It’s a warning sign that Canada’s democracy is losing the trust of its future citizens.

Meanwhile, Canada faces a demographic reckoning. As Baby Boomers retire, health care and pension costs will balloon, to be financed by a smaller, economically strained population.

Younger Canadians, already struggling with stagnant incomes and rising costs, are delaying or forgoing having children altogether. This creates a vicious cycle: fewer workers to support an aging population and an ever-heavier fiscal burden. If left unaddressed, this imbalance threatens not just economic sustainability but trust in Canada’s political institutions.

If these trends persist, resentment among younger generations will likely deepen. Some will turn to political apathy. Others may seek more radical movements or figures that promise to upend a system they see as rigged against them. Once trust in the political system is lost, rebuilding it will be far more difficult than preventing its collapse.

To understand the extent of these challenges, we first need better data that illustrate younger generations’ political preferences and interests. These views should then be more effectively communicated to those in positions of political power – ideally resulting in improved representation. Some activists, notably the think tank Generation Squeeze, are already carrying out this work.

Canada needs a generational reset – one that puts fairness at the centre of political life. Building affordable housing and supporting young families are essential first steps.

The longer Canada ignores generational inequality, the greater the risk of political fragmentation and social anger. A healthy democracy depends on engaged citizens and political trust across generations. Today, this is running dangerously low among our younger people.

Smith School of Business launches new Employee Ownership Research Initiative

November 25, 2025, Kingston (ON) – With three in four Canadian owners set to exit their business within the next decade, Smith School of Business has launched a new research initiative focused on deepening Canada’s knowledge and understanding of a powerful succession model that can enhance outcomes for owners, employees and communities: Employee ownership.

Housed in Smith’s Centre for Entrepreneurship Innovation & Social Impact (CEISI), the Employee Ownership Research Initiative (EORI) aims to shape a ‘Made in Canada’ approach to employee ownership by creating a multi-disciplinary network of academics, researchers, practitioners and businesses. Together, they will fill the gap in relevant data, expertise and business-oriented resources and solutions to support employee ownership activities in the country.

“Amid today’s geopolitical climate and concerns around economic sovereignty, employee ownership can play a crucial role in helping keep Canadian businesses locally owned and creating prosperity for more people,” says CEISI Director Elspeth Murray. “As we experience the so-called ‘Silver Tsunami’, transferring majority ownership to employees, including Canada’s new Employee Ownership Trust model, is a hot topic under consideration, but the process and options are not well understood, especially in a Canadian context.”

That’s about to change thanks to funding support from Jon Shell, a grad of Queen’s University, Chair of Social Capital Partners and board member at Employee Ownership Canada. A prominent advocate for employee ownership in Canada, he has committed $250,000 to assist EORI in conducting research into the impact of broad-based, majority employee-owned Canadian enterprises and government policies to support employee ownership in Canada.

“Employee ownership offers a powerful opportunity to broaden prosperity and strengthen communities,” says Shell. “By grounding the conversation in rigorous research, this initiative will help Canada build an evidence base for a more inclusive and sustainable economy.”

While employee ownership is well studied in the United States and the UK, EORI represents the first comprehensive research initiative of its kind in Canada dedicated to understanding the impact of employee ownership activities and the factors that drive the success of companies owned indirectly through a trust or through the purchase of shares over time.

The multi-year project will establish a national database of majority employee-owned businesses, conduct research and case studies, and share findings through open-access reports, workshops and public events. This work will contribute to a growing movement of companies, scholars, associations and advisors in the employee ownership space, and help shape employee ownership policies and best practices in Canada.

The EORI’s work will be guided by leading academics and industry experts in the field. PhD candidate Lorin Busaan and Associate Professor Simon Pek, both from the Peter B. Gustavson School of Business at the University of Victoria, are joining EORI as research fellows. Pek will also serve on the advisory board alongside Shell and Joseph Blasi, J. Robert Beyster Distinguished Professor and Director Emeritus of the Institute for the Study of Employee Ownership and Profit Sharing at the School of Management and Labor Relations at Rutgers University; Mike Fotheringham, CEO of Taproot Community Support Services; John Hoffmire, Founder of the Center on Business and Poverty, and Research Associate at the Centre for Mutual and Co-owned Business at the University of Oxford’s Kellogg College; and Melissa Hoover, Senior Fellow and Senior Director of the Institute for the Study of Employee Ownership and Profit Sharing at the School of Management and Labor Relations at Rutgers University, and Managing Director of Ownership Culture at Apis & Heritage Capital Partners.

“The research initiative is a big part of creating greater awareness and also the knowledge and know-how for Canadian owners, workers and communities to reap the benefits of employee ownership,” says Murray.

For more information, please visit Employee Ownership Research Initiative.

For media enquiries, please contact:

Smith School of Business

Send media relations a message

Voice: 613.533.2269

Elbows up: Keeping Canadian companies in Canadian hands | Policy Options

By Danny Parys | Part of our Special Series: the Ownership Solution | This post originally appeared in Policy Options

During the Blue Jays’ historic and, subsequently, gut-wrenching run, apparel sales for the team soared across Canada as fans flocked to shell out cash to show their support. Maybe you were one of them.

Maybe you went one step further. Maybe the sole Canadian team’s domination of America’s pastime made you feel a little national pride and, before you headed out to get that new jersey, you pulled on your Roots sweatpants and stopped at Tim Hortons for a double-double on your way to the store.

Then, beside the Jays’ jersey (in this thought experiment there is still a No. 27 Guerrero Jr. in stock in your size) you saw that the CCM hockey stick you really wanted was on sale. Winter is coming, you thought to yourself, so you bought that too.

On your way home, you picked up a case of Labatt Blue, a bag of Miss Vickie’s jalapeno chips (objectively the best flavour) and kicked back to enjoy the game, feeling extra patriotic with all your favourite iconic Canadian brands. Elbows up, eh?

Though if you had done that, the only Canadian brand you would have been supporting in your perfect Canadian day would have been the Blue Jays, a franchise of U.S.-headquartered Major League Baseball.

Indeed, in recent years, many of Canada’s most famous companies and most iconic brands have quietly, but steadily, been purchased by foreign entities. Beyond just superficial wounds to our national pride, the outsourcing of corporate decision-making authority over Canadian companies has been a disaster for workers and consumers.

Policymakers should do more to keep Canadian companies in Canadian hands by, among other things, providing more support to expand financing opportunities and awareness of untraditional ownership models, and beefing up Canada’s net-benefit review requirements.

Declining quality, brand reputation

According to a 2018 Ipsos poll, a whopping 75 per cent of Canadians agreed that the government should do more to stop the sale of Canadian companies to foreign investors.

This should come as no surprise because, after a Canadian brand is purchased by a foreign entity, many consumers notice major declines in quality. Following the sale of Tim Hortons in 2014 to Restaurant Brands International, a firm owned in part by Brazil’s 3G Capital, consumers noticed a deterioration in product quality and the company suffered a steep fall in brand reputation.

Unsurprisingly, as decision-making authority over corporate strategy moves further away from the consumer, brands are less able to respond to the demands of their customers.

Put more bluntly, should anyone be surprised that Tim Hortons hasn’t been able to figure out what Canadians want on their coffee break since being acquired in part by a private equity firm founded by Brazilian investment bankers?

The quiet sale of many Canadian brands has also led to major frustrations for consumers looking to support Canadian-owned businesses.

Trump’s tariffs have caused an uptick in demand for Canadian brands and strengthened desire to support the local economy. However, after further investigation into a brand, many consumers note that behind advertising leaning heavily on Canadian identity and a complex network of corporate holding companies, lies a foreign entity as the true owner.

Workers lose out with distant ownership

Workers are also feeling the impacts as Canadian companies are sold to foreign investors because, as corporate leadership moves further away from the community, so too does accountability, exposing local workers to the demands of foreign executives.

In a recent example, British spirits company Diageo announced the closure of the Crown Royal bottling plant in Amherstburg, Ont., putting 200 jobs at risk and drawing fierce criticism from Premier Doug Ford. Though Canadians might have been outraged, Diageo interim CEO, U.K.-based Nik Jhangiani, didn’t have to look any of the employees in the eye on his way into the office the next day.

And though foreign control of Canadian companies has had damaging impacts on consumers and workers, there is no end in sight.

Instead, foreign buyouts of Canadian companies continue to be a major driver of merger and acquisition activity. In the 2025 second quarter, 25 per cent of mergers and acquisitions involving Canadian target companies were by foreign buyers.

While Premier Ford’s hat might say “Canada is not for sale,” it seems our companies sure are.

Boosting employee ownership

In an era where, for the first time, Canada faces serious economic threats from the United States, one could be forgiven for thinking that now is not the time to restrict investment or foreign access to our economy. But if it means ceding control from Canadian consumers and workers, perhaps Canadians should think twice.

Especially as Canada is facing a major business succession problem; 76 per cent of small and medium-sized business owners plan to exit their business in the next decade.

To ensure these businesses stay Canadian owned, policymakers should be looking at strengthening paths toward employee ownership. Particularly as tax incentives for business owners selling to employee ownership trusts (EOTs) are set to expire in 2026.

Beyond simple tax incentives for business owners, policymakers should look at providing more support to expand financing opportunities and awareness surrounding untraditional ownership models, like co-operatives and EOTs.

While co-operatives and EOTs have proven to be successful in protecting jobs, driving productivity and building wealth for local employees, a chronic lack of awareness holds these models back, preventing more inclusive ownership of Canada’s economy.

For larger companies, the review threshold at which most acquisitions by foreign investors are scrutinized should be lowered, ensuring more foreign takeovers are reviewed before a deal is signed.

What’s in it for us?

The net-benefit-to-Canada criteria should also be broadened to ensure more consideration is placed on local employment and benefits to local consumers.

More stringent regulation should be placed on private equity firms, particularly as their presence expands across the Canadian economy, often by leveraging aggressive tactics to buy up Canadian businesses, such as saddling companies with debt or by consolidating fragmented industries.

Too many iconic Canadian companies have already been sold to foreign investors and Canadians are worse off because of it. More needs to be done to keep Canadian companies just that – Canadian.

Reflections on Budget 2025: Economic growth alone won’t save us

We have taken some time to reflect on last week’s budget.

It is a hopeful budget, with commitments to get big things done. Canada faces real challenges, but we are a big, rich, powerful country. We are the world’s ninth largest economy, respected around the world, with deep commitments to diversity, democracy and the rule of law. Even though Canada faces enormous threats, we should be hopeful.

There are many specific initiatives in the Budget that will deliver real benefits to working Canadians at this time. Strategically, we really like the Budget’s focus on industrial strategy, some tentative steps on making more capital available to a wider diversity of Canadians and commitments to loosen the grip that our oligopolistic sectors have over our economy, which undermines our productivity and make life less affordable for Canadians.

However, we are concerned by the lack of a strategic approach to democratizing the economy and providing more working people and young people a path to wealth, ownership and economic security. While the Budget responds to the wish list that corporate Canada has articulated for several years, there are no guarantees that they will indeed step up to invest – or that those investments will produce growth that benefits working people.

We also note that no sacrifices are being asked of those who can most afford to make them, and very little is being done for the most vulnerable. The era of continental integration and globalization is over. Given the enormity of this geopolitical rupture, and the real suffering that many Canadians and communities are experiencing, more sacrifices could have been required of those of us who can afford to make them.

What we like

A sovereign industrial strategy that helps Canadians benefit from growth

At Social Capital Partners, we have argued that Canada needs more diverse forms of ownership, including public and community ownership of our key resources and assets, so that we have more sovereign control over our future and so that a wider diversity of Canadians can benefit from growth. The government is taking some steps in this direction.

The Budget is clear that the federal government must play a leadership role in industrial strategy and market-shaping activities. There is a recognition that we cannot simply expect capital to flow in productive ways that magically produce good results for Canada or for working people. The creation of new Crowns and agencies to break through regulatory hurdles and ordinary ineffective bureaucratic processes to get infrastructure and resource projects built, and to embed more Canadian ownership in our investments, are important.

In particular, Build Canada Homes, the Major Projects Office and the new defense procurement agency and related initiatives are all welcome. Increased military spending, led by a new defense procurement agency, and expanded partnerships away from the U.S. and towards democratic allies, are also important. Rebuilding our sovereign industrial capacity is a strategic imperative.

There is also a commitment to what appears to be a sovereign fund around critical minerals, which would be a positive step. Canadians should benefit from our own natural resources and steps to make equity investments are positive. We hope that these are first steps towards a more ambitious strategy and that the government can learn from its critical minerals strategy to quickly roll out additional sovereign funds, particularly around manufacturing, food and tech.

In sum, we are pleased to see steps towards an industrial strategy that includes the creation of sovereign funds and a focus on key national imperatives. Along with the Canada Growth Fund and the work undertaken by Canada Development Investment Corporation (CDEV), Canada may at last break free from its deep belief that “capital knows best.” The world’s most successful and resilient democratic capitalist societies understand that governments must shape markets and incent capital in ways that produce broad economic benefits for working people. We may at last be catching up.

Getting capital to the people and places where it will do the most good for Canadians

At Social Capital Partners, we have highlighted that there are many gaps in our private and public financing infrastructure. Capital is simply not getting to enough people, places, businesses and organizations in ways that will create a dynamic, diverse and resilient economy. The government has taken some positive steps.

There is an overall recognition that we need to use our public financing institutions more strategically. The expanded role and budget for the Canada Infrastructure Bank, which delivers public value at low cost, is welcome. Likewise, the commitment to the Business Development Bank of Canada (BDC) to launch a new Venture and Growth fund could be useful, but will require a clearer commitment to concessionary capital – that is, lending at more favourable terms than market rates in order to support other policy goals.

These efforts complement clear commitments around getting more capital to those who have faced barriers to accessing capital in the past. In particular, a variety of commitments to Black and Indigenous businesses, entrepreneurs and communities will deliver returns in terms of growth and inclusion. BDC’s recently announced search fund to finance women to purchase existing businesses is welcome and innovative. The Buy Canada strategy is welcome if it is focused on getting more capital to Canadian-owned businesses, including small and medium enterprises.

In sum, it is good that the government is exploring how it can use its balance sheet to get lower-cost capital to more people in ways that benefit more communities. But overall, these are tentative and underwhelming steps and we hope that, as the government gets more comfortable with concessionary financing, it will use its powers more urgently and ambitiously.

Introducing more competition to help entrepreneurs and consumers

At Social Capital Partners, we have long argued that Canada needs more competition, which should produce more innovation, productivity and growth. More competition will also create more pathways for Canadian entrepreneurs to enter and disrupt markets, and bring down prices for Canadians.

The Budget takes tangible steps towards open banking and confronting the oligopolistic banking sector. The Budget commits to legislative changes that will make it easier for federal credit unions to scale and for provincial credit unions to grow. There are commitments to review bank and Interac fees (but we have heard those before). These should help Canadian consumers and businesses. The commitment to non-compete clauses in federally regulated sectors is also good for workers and a more competitive economy.

In sum, there are many references to a more robust competition agenda and some tangible steps, but there is much more that needs to be done. In particular, it would be good to empower the Competition Bureau to confront the serial acquisitions and business roll-ups going on in communities across the country that optimize for short-term profits and, in turn, make life less affordable, suppress wages and enrich the wealthiest.

Notable for their absence

Legislative and policy changes to support a sovereign Canadian business transition strategy

Trillions of dollars in baby boomers’ business assets are going to change hands in the coming years. These assets could transition to young Canadian entrepreneurs, not-for-profits, social enterprises and Employee Ownership Trusts (EOTs) through targeted programs and concessionary capital offered by BDC or another agency. This is a generational opportunity that could shape our economy and democracy for the next half century. It is one of the best things we could do to democratize the economy and prevent control of Canadian assets from drifting into the hands of American private equity funds.

New community financing infrastructure

Although there were some moves towards getting more capital into the hands of Canadian entrepreneurs, a strategy to finance smaller businesses, social enterprises, not-for-profits, co-ops, care providers and community organizations was absent. The community finance and social finance sector – and the networks of people, businesses and organizations that rely on them – have developed low-cost, scalable projects that require investment. All of the arguments used by the government in favour of catalyzing big pools of capital to invest in big projects apply equally well to mobilizing capital in favour of local, community projects. Canada needs new mechanisms and facilities to deliver concessionary capital and loan guarantees and these are essential to economic resilience, well-being and sovereignty. This gap in the Budget reflects a wider reality that the government has no strategy to support, engage or mobilize the not-for-profit sector.

Intergenerational equity

The Budget has little to say about the real concerns of younger Canadians. While there are some bits and pieces around summer jobs programs, this budget has no coherent or substantial approach to creating a more hopeful future for young Canadians. This is a reflection of a broader absence of focus on human capital and investments in education. And the housing measures are underwhelming, including the refusal to confront the asset inflation caused by wealthy investors in residential real estate. The Budget offers little other than vague hopes that jobs will be created sometime in the future due to private-sector investment. At SCP, we believe it is time to free up revenue for more investment in young people. We can find those resources easily by eliminating the age tax credit, eliminating the boost to Old Age Security (OAS) at age 75 and starting the claw-back of OAS at lower levels.

Renewal of the tax incentive on Employee Ownership Trusts

Making it easier for business owners to sell to their employees, and eliminating the financial hit they would otherwise take in doing so, is one of the most important things we can do to democratize the economy and access to wealth for many Canadian workers. The government has taken significant steps over the past two years to make the employee ownership movement a reality. The government is now threatening this progress by not making permanent its soon-to-expire tax incentive. Business transitions take time to plan and the tax uncertainty that the government is creating by sunsetting the incentive after December 2026 – before the model has even had a realistic chance to take off in Canada – will lead to more businesses being sold to American private equity or competitors. The government still has time to rectify this issue, but time is running out.

Incenting or requiring philanthropic and pension fund capital to invest more in local Canadian impact

There are some signals in the Budget that the government understands that big pools of Canadian capital should be investing more to advance community well-being and local impact. But this is mostly framed as increasing investments in infrastructure like airports, not local businesses and community infrastructure. If Canadian pools of capital continue to invest so little in domestic businesses, the government – and beneficiaries – will need to stop asking nicely.

A digital sovereignty and democratic resilience plan

Big American tech firms are undermining Canadian democracy, poisoning our information ecosystem, hurting our young people and cannibalizing Canadian businesses. The Canadian government continues to support them, patronize them and subsidize them in various ways. Meanwhile, the global authoritarian right is running a pretty standard playbook to undermine democracies around the world, including Canada. More resources and tools need to be mobilized today to protect us from these active threats. The Budget says “AI” a lot but offers few specifics on what the government will do to combat these threats to equality, democracy and our humanity.

What next?

We understand that this Budget is primarily focused on responding to corporate Canada’s long-standing complaints that the investment climate in Canada is not good and that the regulatory environment makes it too difficult to build things. We will soon see whether this Budget catalyzes the private sector to invest in Canada’s future and whether those investments produce sustained economic growth.

But we were disappointed that there was so little about how to ensure whatever growth does occur delivers widespread benefits to Canadians, workers and young people. Canada is experiencing the end of the economic and geopolitical security orders on which we have relied and in which we have thrived.

We believe we need even more ambition and creativity in our responses to this rupture. Unleashing private-sector capital investment in big projects will not be enough. We need new playbooks, deployed more aggressively, with the goal of mobilizing all of society, not just large private-sector players.

There are specific initiatives that will help working people and the most vulnerable – the National School Food Program and automatic tax filing, for example. But these do not speak to the structural elements of the economy, which increasingly see benefits from economic growth flowing upwards towards fewer interests.

The Budget talks about “sovereignty” and “control over our future,” but its prime directive is ‘growth.’ If we are to bend the curve on the current trajectory of both capitalism and democracy, we need economic growth that does not perpetuate grotesque economic inequality or make life less affordable for working Canadians.

There are tools available to the government to prevent these outcomes if they choose to use them. We hope they will soon start to deploy them in a more sustained, intentional way.

Budget 2025 did not extend the $10M capital-gains exemption for sales through EOTs

Statement from Employee Ownership Canada

Budget 2025 and the Future of Employee Ownership Trusts in Canada

We share the disappointment felt across Canada’s business and advisory community that Budget 2025 did not make the $10 million capital gains exemption for sales through Employee Ownership Trusts (EOTs) a permanent feature of Canada’s tax system. The current incentive, passed only in 2024 with an expiry set for December 2026, means that the business community has not had adequate time to act.

This decision creates uncertainty for many business owners and advisors preparing for ownership transitions that often take more than a year to complete. The exemption was designed to make it easier for business owners to sell through an EOT, keeping jobs, ownership, and prosperity rooted in local communities. Without it, some owners may delay or reconsider transition plans, slowing the broader shift toward employee ownership.

Even so, there is reason for optimism. The August 2025 legislative updates, continued cross- party support, and strong engagement from business owners, employees, and advisors all point to growing recognition of the value EOTs bring to Canada’s economy.

We remain committed to working with government and partners across the ecosystem to make the capital gains exemption permanent, ensuring employee ownership trusts remain a viable, long-term option for Canadian businesses.

Employee ownership is more than a policy. It is a pathway to shared prosperity, inclusive growth, and resilient local economies. We’ve seen how this model can preserve legacies, empower employees as co-owners, and strengthen communities. In the United Kingdom, where EOTs have been supported through permanent tax incentives, a business is sold to an EOT every day.

As we look ahead, we call on our members, partners, and champions to continue advocating, educating, and building awareness to demonstrate why expanding employee ownership is not just good for business, but essential for Canada’s economic future.

To become an EOC member or learn more about the benefits of Employee Ownership Trusts for Canada’s economy, visit www.employee-ownership.ca.