Hype or help? Can crypto and stablecoins solve economic inequality?

By SCP Fellow Dan Rohde

Cryptocurrencies, like Bitcoin, are caught between two worlds. On the one hand, they fancy themselves “currencies” – promising to be an effective means of payment. On the other hand, cryptocurrencies act as speculative assets – things purchased today with the hope that they will increase in value down the line.

The problem is that these two functions often conflict with one another. And while crypto assets have proven effective speculative assets (indeed, they’ve made some speculators quite a lot of money!), they’ve proven quite bad as a means of payment. Exchanges, and stablecoins, are the primary means by which crypto advocates are attempting to bridge this gap – to move from the world of speculation to a functional means of payment. Sadly, the result leaves much to be desired, and, in my opinion, adds rather little to our existing payment infrastructure.

This hasn’t stopped advocates, like Mike Moffat, from promoting the use of stablecoins as a common currency. His argument is that this new currency could help the cost-of-living crisis and promote economic equality – particularly for young people. I am not convinced that crypto can help address economic inequality. Before we get into that, let’s break down what stablecoins are and aren’t, and how to think critically about their promises.

To be effective, a currency should have at least two things. First, it should be an easy mode of payment. If it’s a pain to use something to buy and sell things, you’ll typically use something else. (For example, the easier debit and credit cards have become to use, the more they displaced cash as a mode of payment.)

Second, it should have a relatively stable nominal value. It’s vitally important to know, when you go purchase a coffee, that the toonie in your pocket will actually buy you that $2 coffee without haggling or negotiation. In other words, the number on your money should generally be what it’s worth in purchases. The more variation you have, the harder it is to use your money as a means of payment.

Cryptocurrencies are generally very bad at both of these: here’s how. Bitcoin, just to take a well-known example, distinguishes itself by saying that it’s a fully anonymous means of peer-to-peer payment that does not require financial intermediaries, like banks or credit card companies. It casts itself as “digital cash” that you can exchange directly with your peers. To accomplish this, it uses elliptic-curve cryptography to anonymously process payments between digital wallets – a process that requires so-called “miners” to expend considerable energy and computing power to validate each transfer. While estimates vary, one study suggested a single bitcoin transfer can require between 100 and 1000 kWh, compared to .001kWh for a credit card purchase. (This means that a single bitcoin purchase can take around 500,000x more energy than a credit card purchase!)

The time involved in processing a crypto payment is also substantial: Bitcoin payments can get confirmed in about 10 minutes, but typically take 1-1.5 hours to complete. Imagine waiting 10 minutes to confirm payment of your coffee. For this reason, bitcoin transactions very often occur over a crypto-exchange. (Imagine a stock exchange, but for crypto assets.) This greatly simplifies the process of moving assets between holders, but it also does away entirely with that idea of bitcoin being anonymous and independent of financial intermediaries.

Cryptocurrencies are also notoriously bad at holding a stable nominal value. Like all speculative assets, their value rises and falls continuously based on available prices on the market. At any given moment, you don’t know exactly how many $2 coffees your bitcoin will buy you. At the time I am writing this, one Bitcoin, or “Btc,” is valued at about $114,000; exactly 4 hours ago, it was just over $112,000; six months ago, it was $75,000. This kind of variability is fine when you’re playing the markets, but it’s terrible for making everyday payments.

Stablecoins were developed to overcome these problems. A stablecoin is a type of crypto asset that, unlike Btc, isn’t anonymous, peer-to-peer or even necessarily protected with any sort of cryptography. Rather, a stablecoin is issued by a private company, and pegged to a regular fiat currency (like the U.S. dollar, or USD). What does it mean that the coin is “pegged” to a regular fiat money? All it means is that the issuer promises their coins can be redeemed at any time for their face value in regular money. So, one USD-pegged coin can be redeemed for $1 in your bank account. Stablecoin issuers maintain this peg by holding a set of liquid financial assets that they can sell off at any time to ensure they have enough money to pay out redemptions. Placing stablecoins on an exchange where they can be easily swapped with crypto assets like bitcoin aids in converting crypto-assets into regular money and helps anchor their nominal value.

If this stablecoin setup sounds vaguely familiar to you, that’s because it is: it’s exactly how your bank works! Your bank issues credits denominated in Canadian dollars, or CAD. They don’t call those credits “coins,” but that doesn’t matter very much. Your bank ensures that the credits they offer (which we call “deposit accounts”) stay pegged to CAD by holding a large, diversified set of liquid financial assets, by subscribing for deposit insurance under the Canadian Deposit Insurance Corporation, or CDIC, and playing a part in Canada’s financial safety net.

However, there is one big difference between your bank and a stablecoin issuer: your bank is tightly regulated under the Office of the Superintendent of Financial Institutions (OSFI) and the Financial Consumer Agency of Canada (FCAC) and can turn to the Bank of Canada in a crisis. In contrast, your local stablecoin issuer is likely trying its best to avoid any and all such regulation as far as it is able. You can hope they are being honest about their assets, but all you really have is hope.

Like many pieces about crypto and stablecoins recently, Moffat’s blog points to many, very real problems with our current financial system. He points out how expensive credit card transactions are for small businesses, and how difficult it can be to transfer money abroad. (Here, for example, is an excellent recent article about credit-card fees.) These are very real problems, ones that particularly affect small business, and that call for real solutions. He also points to a very genuine and important ambiguity as to how stablecoins should be regulated – either under the Federal Government’s power to regulate ‘banks’ or under the provincial power to regulate ‘securities.’

The big question, however, is what crypto actually does to solve these problems.

Moffat says that stablecoins can be programmed/designed to provide cheaper payments and higher rates of interest for young and middle-income savers. He doesn’t specify anywhere exactly how or why they don’t already do this. What type of “programming” is going to make lending to younger or lower-income individuals profitable for stablecoin issuers or crypto lenders when it isn’t for banks? How is it that stablecoin issuers, which adopt much of the model of regulated banks, could offer more “frictionless” payments than the existing payment system? How exactly are stablecoins, which are tied to notoriously volatile crypto markets, going to help younger individuals save safely for a home?

Advocates often wax lyrical on crypto’s potential to usher in economic equality, and they often build their case on very real problems with our financial and payments system. But we should not so easily buy into their myths. While I’m not making any claims about Moffat in particular, advocates are very often (though not always) out to hype their product rather than advocating for real solutions to these problems. We should always ask whether what they are offering actually adds anything of value to be considered.

There are no doubt real problems with our current banking system that contribute to economic exclusion and inequality. As Moffat points out, fees for international remittances are large. Too many Canadians are “underbanked,” denying them access to vital payments and lending infrastructure. Rather than turning to crypto, which was founded on libertarian anti-government ideology, there are other potential solutions to these problems.

Canada could directly regulate credit card fees or international remittances to help consumers, small businesses and people sending money to family abroad. Open banking also provides an avenue to rethink public access to credit. Lastly, but perhaps most importantly, we could (and should) consider developing a public digital currency, such as a Central Bank Digital Currency (CBDC). Why shouldn’t the state, which already provides cash free of charge, provide a public, digital money? A type of debit card that small businesses can accept without paying fees to banks. Wouldn’t that address many of the main issues with our current system without turning to digital libertarians?

At best, stablecoins mimic what our banks already do, only with less transparency and oversight. If we want a payment system that is cheaper, fairer and more inclusive, we should look through the hype to real policy innovations to deliver genuine improvements for Canadian households and businesses.

Budget 2025 should bolster employee ownership to strengthen Canada’s economy | Canadian Dimension

By Simon Pek, Lorin Busaan and Alex Hemingway | This post first appeared in Canadian Dimension

In his first post-election news conference, Prime Minister Mark Carney made a bold commitment to “take control of our economic destiny to create a new Canadian economy.” If that is to happen, Canadian employees deserve more than inspiration—they deserve a greater ownership stake and voice in the companies where they work.

In Budget 2023, the federal government enabled the creation of employee ownership trusts (EOTs), which can purchase and hold shares of businesses in perpetuity on behalf of employees. Unfortunately, the associated capital gains tax incentive was limited to three years and will expire in 2026. Budget 2025, expected this fall, is an opportune moment to make employee ownership permanent by extending and expanding the capital gains exemption for EOTs.

Employee ownership trusts are one model among several of broad-based employee ownership, and empirical research from around the world shows they have strong benefits for firms, employees, and the broader economy: greater resilience, improved productivity, reduced inequality, and stronger continuity in business succession. For example, a recent UK study found that companies converting to employee ownership via EOTs have, on average, enjoyed a 4.4 percent higher productivity increase over three years compared to similar firms.

Early conversions in Canada—at companies like Taproot Community Support Services, Brightspot Climate, and Grantbook—suggest strong interest among both business owners and employees in this model. Based on the highly successful UK experience, it is plausible that hundreds—if not thousands—of conversions could eventually take place here. In the UK, much of the uptake has been driven by deliberate policy decisions: generous tax relief, clear regulatory definitions, and awareness-raising among business owners.

Canada’s federal government has made a promising start with the temporary capital gains exemption—but with limits. The exemption on the first $10 million of capital gains for business sales to EOTs is important. Yet many EOT transactions take more than a year to plan and complete. If the incentive expires prematurely in 2026, many potential transitions may be abandoned or indefinitely deferred.

To avoid losing momentum, Ottawa should extend the capital gains exemption indefinitely rather than letting it lapse after only two years. A permanent exemption would give business owners certainty and allow longer planning horizons, encouraging thoughtful, sustainable conversions instead of rushed ones. Just as importantly, the exemption should be broadened to include worker cooperatives. Budget 2024 proposed such an extension to eligible worker cooperative corporations, but that legislation was never finalized. Worker co-ops are a long-standing model of employee ownership in Canada, offering employees direct control rights and a tradition of democratic governance that complements the EOT framework.

The cost to the federal government is modest. The Office of the Parliamentary Budget Officer has estimated foregone tax revenues from the temporary EOT exemption at approximately $7 million per year. Compared with other tax exemptions—such as the principal residence exemption, which costs the federal and provincial governments billions annually—this is minimal. Even if extended to include worker co-ops, the revenue impact would remain limited relative to the economic and social benefits generated.

Those benefits are substantial. Firms that convert to employee ownership tend to be more resilient in economic downturns, with lower incidence of layoffs and closures. Evidence from the UK shows employee-owned businesses are far less likely—by a factor of five—to lay off their staff over a three-year span than comparable firms. Employee ownership also supports stable employment in smaller communities, strengthening Canada’s economic sovereignty by keeping ownership and decision-making local.

Workers gain too—not just through job security but through income and wealth accumulation, particularly for groups facing economic exclusion. US studies show that employee ownership reduces wealth gaps, boosts household incomes, and gives workers a direct stake in profits. The social dividends extend beyond pay: employee-owners often report higher morale, greater civic engagement (including higher voting and volunteering rates), and stronger commitments to environmental practices within their firms.

Canada is at a pivotal moment. More than $2 trillion in business assets are projected to change hands in the next decade. This demographic shift, with retiring business owners seeking succession paths, creates a rare opportunity to shift large swathes of private enterprise toward employee ownership. If Budget 2025 extends and expands the capital gains exemption, this would be a powerful lever: enabling business succession that preserves jobs, strengthens communities, and shares wealth more broadly. Such a policy would likely enjoy support across the political spectrum and from the business community, and could be a quick win for Canada’s economic sovereignty.

Simon Pek is an associate professor in the University of Victoria’s Gustavson School of Business.

Lorin Busaan is a PhD candidate at the University of Victoria’s Gustavson School of Business.

Alex Hemingway is a senior economist at BC Policy Solutions.

What being an employee-owned company means to me

By Social Capital Partners

On a personal level, when you “take ownership” over something, it means that you take responsibility for your actions, ensure tasks are completed and goals are met.

You feel accountable for that effort’s success.

While company governance is not often what employees think about in their day-to-day work lives, “taking ownership” of the company you work for can result in some of those same good feelings.

For what it’s like to be on the inside of an employee-owned company, we spoke to a few of the 750 employees who recently became 100-per cent owners of Taproot Community Support Services—a social services provider across B.C., Alberta and Ontario.

“We’ve worked hard, so it’s really nice to be rewarded for that, especially as frontline workers,” said Talica Bautarua, a residential worker at Taproot. “It feels like we’re in it together more now.”

The rewards that Talica is speaking about include company morale and spirit, for sure. They also include financial rewards paid to each employee as dividends each year. Last year, each employee would have received about $1000 to $1500 on top of their salaries—and as the company succeeds over time, the employees will share financially in Taproot’s success.

For Andrew Achoba, a program director and one of the three new trustees of the Employee Ownership Trust (EOT), this speaks volumes about the organization’s values.

“As someone who works closely with caregivers and families in northern Alberta, I see daily how strength is built when people work together. The employee ownership trust reflects that same principle of ownership shared, accountability shared and success shared.”

Their colleague Tracy Atkin, director of specialized services and a member of the Taproot board has thought deeply about how this transition to an EOT is a deep reaffirmation of “who we are and what we stand for.”

She recalls that the decision to transition to an EOT was not made lightly and took at least a year of thought and considering options.

“Looking back, our Board and shareholders faced critical choices along the way. Choices that made us think about our values: choices for other ownership structures, like selling out to a larger corporation or concentrating on share sales; these options would not have expanded our ownership group and honestly, risked losing sight of why we do this work. Once we decided on the EOT, distribution [or how the ownership would be shared among employees] needed to be sorted out; distribution could have looked very different with many structures prioritizing positions, titles or tenure. Time and again, the Board chose to prioritize Taproot employees. We also achieved a 100% transition to the EOT, meaning 100% of our shareholders believed in this. We’re all in,” she explains.

But Tracy also gets the example that Taproot is setting for other Canadian companies and the broader economy.

“This is significant because we live in a world where capitalism places profit above people,” she says. “That profit often filters up to the top—and we chose a different path. We embraced a model that prioritizes people first and I am so proud of the committee that took that to the extreme and decided to provide equal ownership for everyone regardless of position. But this isn’t just a financial decision; it’s not just a structural shift; it’s a moral one. It’s reimagining what success in business can be. No other business in Canada has done this. Success doesn’t have to mean getting up to the top 1%—hearing our employees’ excitement in the kickoff meeting, that is success.”

And as Taproot moves forward, the people who work there hope that their story inspires other companies to explore an EOT.

“What’s especially powerful for me is how this journey aligns with Indigenous governance values,” says Tracy. “I am proud to have been part of the Board that voted on this transaction. Indigenous leadership teaches us to lead from within, to walk with our people, never above them. It is rooted in relationship, reciprocity and responsibility to each other. These principles were present throughout this entire process, and I am incredibly proud of the people that made this happen.

This transition is bigger than us—I think it is a call to other organizations to redefine success in business, I think it is a move against capitalist structures and I think investing in people uplifts our communities and creates a legacy of shared impact that we all get to be a part of.”

To learn more about employee ownership and Employee Ownership Trusts, please visit www.employee-ownership.ca

Wealth inequality in Canada is far worse than StatsCan reports

By Dan Skilleter | Part of our Special Series: Always Canada. Never 51

The nation’s fiscal fact-checker, the Parliamentary Budget Officer (PBO), takes aim at the severity of wealth inequality in Canada in a new report. This is the third time the PBO has run the numbers since 2020 and the report shows just how much of Canada’s wealth is concentrated in a tiny circle of families.

The fresh analysis, using updated survey data from Statistics Canada, reaffirmed the dramatic lopsided shape of our economy—one where the top one per cent of families own nearly one quarter of all the wealth in the country, and where the top five per cent own over 40 per cent.

It’s unusual for an independent office like the PBO to take the time to repeatedly publish updates of a study like this. So why do it, then? It’s because StatsCan’s “official” data on the state of inequality in the country are flawed and misleading—but the government keeps publishing those numbers anyway.

We know why the government’s official numbers are so misleading. When Statistics Canada interviews a sample of Canadian families every few years to get a picture of what they own, the list of families contains a curious omission. They don’t talk to any of the richest families.

No effort is made to ensure that the richest families even get a request to participate—before even factoring in that participation is purely voluntary and these families are the most likely to decline such an interview. Statistics Canada does not correct or adjust for this.

So, the government’s best available data on Canada’s wealth gap excludes, by design, the wealthiest families in the country. If we didn’t have the PBO fact-checking Statistics Canada’s work, the numbers would tell us the top one per cent own only 2.5 per cent of all wealth – not nearly 25 per cent of all wealth in Canada, as the PBO reports.

And without the resources and authority to conduct surveys, the PBO’s only means to get at the real wealth of those richest families is to incorporate data from the “rich lists” compiled by media outlets like Maclean’s or Forbes – reporting that undoubtedly understates the true wealth of these families, due to how much of their personal financial information remains out of public view.

While not a perfect measure, the PBO’s numbers are closer to the truth, and their fact-finding persistence will continue to be necessary until our government gets its act together.

As I argued in a 2024 report called Billionaire Blindspot, Canadians live with a false sense of comfort—or even smugness—about how equal we are. While we have our inequalities issues, we think of ourselves as a beacon of egalitarianism compared to our neighbours to the south.

We tell ourselves “At least we’re nothing like them,” and we have official government statistics to back us up. But as I showed in my report, when you add in what we publicly know about Canada’s richest families, as the PBO took it upon itself to do, the concentration of wealth here looks quite similar to the U.S.

It’s insulting that Canadians are forced to rely on the PBO’s continued interest in wealth disparities across our population for the public to get sporadic glimpses of reality. And it’s deeply problematic that our official statistical agency is perfectly fine with misleading Canadians.

It’s time for our government to get serious and take on this vital monitoring work itself. Wealth distribution is a core measure of our country’s health, given that pronounced economic inequality is linked to lower long-term GDP growth rates, higher crime rates, poorer public health, increased political polarization and likelihood of financial crisis.

Other countries, like the U.S., make sure their measures include interviews with the wealthiest families, making their data much more reliable than ours. Failing that, Statistics Canada should find credible external sources to undertake the modelling work rather than requiring the PBO to step in to provide more accurate and useful measures of wealth inequality in Canada.

Watch the video: Is Canada's wealth gap really as bad as the U.S?

As Canadians, we like to think we’re strong and free. But, when it comes to the wealth gap, we’re looking more like America Lite—better manners, but almost all the inequality. The way our economy is set up means that most of the benefits from economic growth go to financial interests and speculators, rather than to workers or other businesses. We can shift economic power to more people and aspiring entrepreneurs by making them owners. When more people have a stake, Canada’s economy works better for everyone—not just investors.

Build, baby, build. Or sell, baby, sell? Canada should reject Sunoco's takeover of Parkland | Policy Options

By Sarah Doyle and Jon Shell. This post first appeared in Policy Options.

U.S. President Donald Trump’s tariffs, threats to annex Canada and musings about the use of economic force against us are shaking the foundations of our economy.

This is not just another storm to be weathered. It demands a rethink of how Canada engages with the U.S. and the world, including how we approach foreign direct investment (FDI).

In March, in response to U.S. threats, François-Philippe Champagne, then the federal minister of Innovation, Science and Industry, tightened Investment Canada Act guidelines to protect against “opportunistic or predatory investment behaviour” by non-Canadians.

Those guidelines are facing an early test now because shareholders of Parkland Corporation, Canada’s largest gas station operator (whose brands include Ultramar, Pioneer, Chevron and On the Run), recently voted in favour of a takeover by U.S.-based Sunoco LP. Under the act, Ottawa can approve or reject the deal.

The Parkland deal may be attractive to the government because it offers US$9 billion to add to Canada’s total FDI, which politicians often tout as an indicator of national economic health. However, due to its volatility and concentration in a few sectors, total foreign direct investment is not a good reflection of the underlying strength of the economy.

In the current context, geopolitical objectives should be paramount. Transactions that transfer control of important Canadian companies to countries with which we are in economic conflict, such as the proposed Parkland acquisition, should be rejected by Ottawa.

This deal would bring none of the benefits typically associated with FDI. It is unlikely to lead to increased capital investment, more or better jobs, or technology transfer into Canada. In fact, its impact may be just the opposite.

The federal government is leaving investment dollars on the table—but it can fix that in the budget

By Matthew Mendelsohn | Part of our Special Series: Always Canada. Never 51

At Social Capital Partners, we have watched the community finance and impact investment markets grow over the past 25 years.

The federal government has played a key role in this evolution at critical moments. The Task Force on Social Finance in 2010 represented an important agenda-setting breakthrough and the creation of the Social Finance Fund in 2019 was a crucial market-shaping policy initiative that drew more capital to the sector.

Throughout this period, investors, philanthropists and creative community leaders built new instruments and new markets to deliver social, environmental and local returns, often in the face of bemusement from traditional finance.

But gradually, and as the enormity of the crises we face has become more apparent, these ideas are becoming mainstream.

More and more asset owners are committed to investing in the social, economic and environmental transformation required at this moment in our history, and more and more instruments, such as community bonds and local impact investment funds, have come online. This was clear at the recent Victoria Forum, where community and philanthropic leaders joined together and outlined creative and viable ideas that were unthinkable two decades ago.

Likewise, the many 2025 federal pre-budget submissions from the social finance community reinforce the vision and possibility of this moment. SVX, Definity Foundation, Raven Indigenous Outcomes Funds, Rally Assets, Relèven, Catalyst Community Finance, Impact Guarantee, the Table for Impact Investment Practitioners, Philanthropic Foundations of Canada, Employee Ownership Canada and our own at Social Capital Partners, amongst many others, have highlighted some of these proposals.

These investments are no longer curiosities or pilots to explore, and the finance and community leaders driving these changes don’t want pats on the head. The ideas are scalable and transformative, and the leaders are ready to step up to support Canadians and the economy at this moment. They must be an essential part of the federal government’s strategy to confront the rupture in the global economic and security system through which we are living.

Philanthropic leaders are ready to step up in a transformational way. Private capital is increasingly interested—but needs some more enabling support from government.

I understand that the government’s first priority is mobilization of private pools of capital for big national infrastructure and resource projects. But the government needs to apply the same logic and focus that they’re deploying for big energy projects to mobilizing capital to invest in local Canadian businesses, social purpose organizations and community infrastructure.

The vast majority of the Canadian economy does not strive to export goods or services. Most businesses serve their local communities and are not directly exposed to trade or tariffs. Of course, the government must help those sectors and workers who are being hit by Trump, but we can also strengthen those sectors that are vital to our economic resilience in the face of attacks on our export sectors. Holders of capital want to invest in local businesses, affordable housing and community infrastructure. Catalyzing these kinds of investments will drive sustainable and inclusive economic growth and help real people. These investments act as economic stabilizers in communities impacted by tariffs. They create hope and opportunity for young people.

At a time when governments are being careful with every dollar of public expenditure, the social finance community is rising to the challenge and putting forth proposals that highlight how the magic of finance can be used to deliver social and economic benefit for very little risk or investment on the part of government. The government knows this is true for large private investments in natural resource and infrastructure projects. I hope they have internalized that the logic applies—and the people and capital exist—for community and local investment as well.

And that is the main takeaway I have from reading the Budget submissions and hundreds of conversations over the past year: despite the growing maturity, size and track record of success within the social finance community, we still need better social and community financing infrastructure and more enabling policy and legislative signals. This would allow good social finance investments to properly scale and deliver the kind of outsized impact that is needed at this time.

What would this look like in practice? I believe the government should be signaling its intent to consult on:

- the accreditation and capitalization of community finance institutions,

- the formalization of loan guarantee facilities and co-financing approaches to de-risk projects, and

- legislative and tax changes that will incent and require more philanthropic and private capital—including pension fund capital—to invest at home and in local communities.

Whether focused on housing, climate, food systems, poverty reduction, succession planning or local economic development, organizations are leading transformative work that is directing capital in ways that serve communities and long-term economic resilience rather than short-term profit. Social finance, impact investors and transformational philanthropy organizations are looking to the federal government to create the conditions for increased investment.

The federal government has already demonstrated creativity in using financing in more ambitious ways. The Business Acquisition Loan for Indigenous Communities is one recent example. And earlier this month, the Prime Minister announced that “low-cost capital” will be available to businesses that have relied most heavily on trade with the U.S.

Many more opportunities exist, but they are constrained by fragmented financing and outdated regulatory frameworks. It is time for the federal government to step up and make it easier to invest in local businesses and Canadian community economies.

I hope the federal government sees what is happening on the ground in Canada, in communities and with asset holders—and acts accordingly. Building the right policy and financing architecture to support community investment will catalyze more investment, make a material contribution to economic growth, deliver real public value and improve our economic resilience and sovereignty.

There really is no reason not to get moving on this agenda.

Acquisitions can’t build Canada: Understanding Foreign Direct Investment in an age of geopolitical fracturing

By Sarah Doyle and Jon Shell

In last year’s budget remarks, former Finance Minister Chrystia Freeland celebrated the “significant accomplishment” that Canada’s per capita foreign direct investment (FDI) was the highest in the G7, “driving growth, increasing productivity and boosting innovation.” She is far from the only politician to frame total FDI as a positive indicator of economic health, but this masks a more complicated picture.

Total FDI does not actually tell us much about the state of the economy. One large deal can significantly affect total FDI inflows, which can vary dramatically from year to year (swings of 40% are normal). Each deal will depend on idiosyncratic, sector- or company-specific considerations that are often disconnected from underlying national economic trends. Moreover, not all FDI is created equal.

FDI is a jumble of different types of investments with vastly different impacts on the Canadian economy–some clearly positive, some negative and some a mix of both. The category that raises the most questions, and that is the focus of this piece, is that of cross-border mergers and acquisitions, or M&A.

Understanding these nuances is important. Because FDI is used as a shorthand measure of economic health, it is simply assumed that more FDI is good for economic growth, productivity and business investment. And that makes it difficult for politicians to reject FDI transactions that undermine the wellbeing of Canada’s economy and workers. The ability to distinguish between beneficial and harmful FDI is even more important now, in the context of a global trade war and threats to Canada’s economic sovereignty.

In this explainer, we aim to unpack FDI: what it is, when it is and isn’t beneficial and why understanding these nuances matters.

What is Foreign Direct Investment?

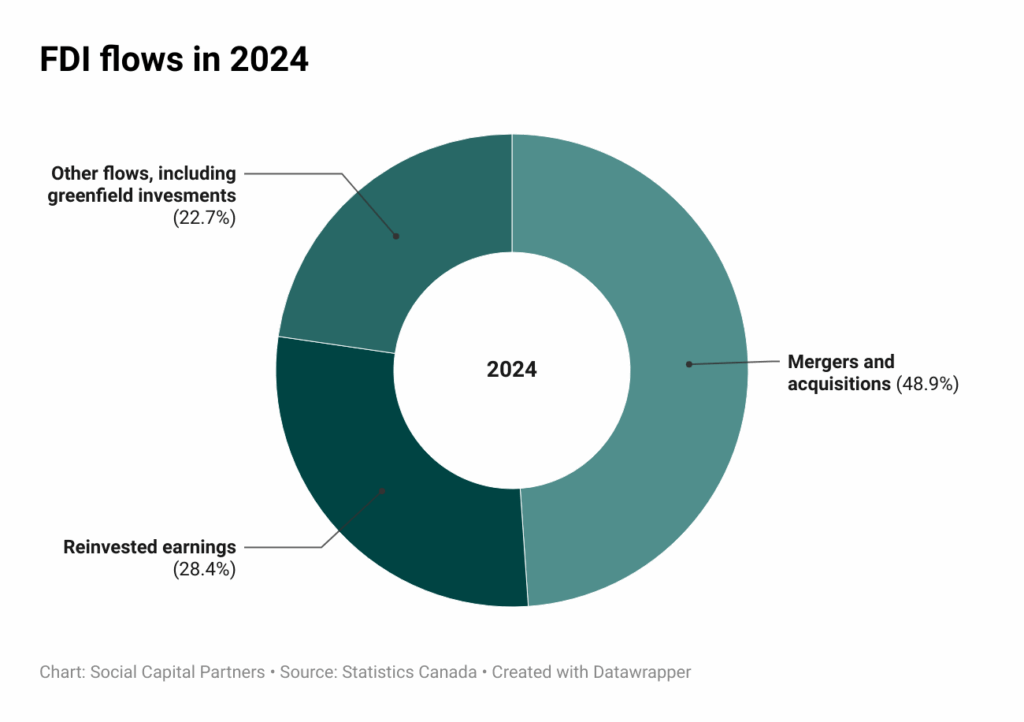

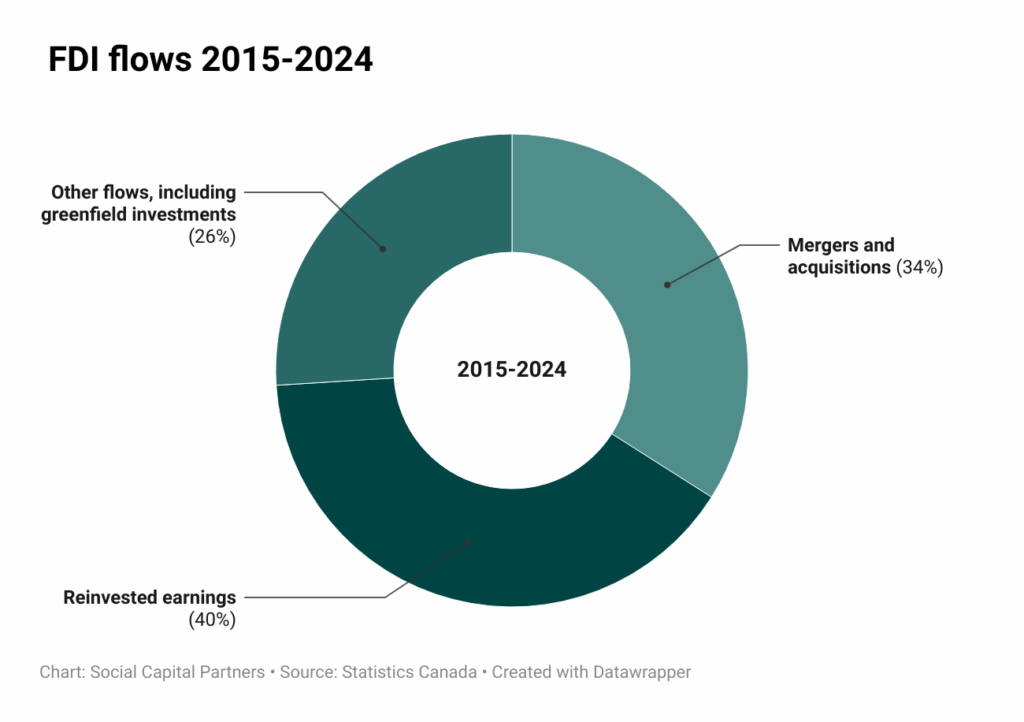

FDI occurs when an investor from one country owns at least 10% of an entity in another country. Statistics Canada breaks FDI down into three categories: M&A, reinvested earnings and “other flows.”

When we think of FDI, we typically imagine foreign capital enabling a new manufacturing plant to be built from the ground up. This is actually the rarest of the three main categories of FDI, often called “greenfield” investment. It’s included in the “other flows” category in Statistics Canada’s accounting, which on average has made up 26% of Canada’s inward FDI over the last 10 years (and includes a grab-bag of other transactions, like intracompany loans).

The biggest category of FDI inflow (40% between 2015-2024) is from foreign-owned companies keeping profits i Canada that could otherwise be sent to the owners as dividends. Whenever this money is kept in Canada, it’s called “reinvested earnings.” This might mean new capital investment, which could look a lot like greenfield FDI. But it also includes other things, like holding cash on the balance sheet to be sent out later as dividends. This category is included in FDI as an accounting convention but often isn’t very different from Canadian-owned companies retaining earnings for investment or other purposes. Because this category generally doesn’t give rise to contentious policy questions, we don’t dig deeply into it in this piece.

The final category is mergers and acquisitions, or M&A, where a foreign investor acquires at least 10% of a Canadian company. Over the last 10 years, this has accounted for 34% of all FDI (see Graph 1), and in 2024 accounted for almost half (see Graph 2).

Graph 1: Graph 2:

Graph 2:

The benefits of FDI

A typical definition of FDI will include a list of its many benefits to a country’s economy. In addition to supplementing domestic business investment (which is perennially lagging in Canada), FDI is said to create well-paid jobs, catalyze innovation spillovers and increase productivity from leading global companies bringing cutting-edge technology to Canada, connect local businesses to global supply chains and emerging markets and generate net-new economic activity and assets that contribute to GDP growth.

When describing these benefits, politicians, commentators and government agencies tend to focus on total FDI. Greenfield FDI does indeed hold the promise of delivering on these benefits, but they are far less likely in the case of cross-border acquisitions (M&A), which in many cases will have the opposite impact. Understanding these differences is critical to making informed policy decisions.

To unpack these differences, we’ll look at how greenfield and M&A FDI might deliver on the presumed benefits: investment capital, jobs, growth, innovation, productivity and access to new markets.

Greenfield FDI

Greenfield FDI is “where the magic of economic development really happens” according to the Financial Times fDi Intelligence team. The term “greenfield” is meant to describe the building of something new, where nothing previously existed – i.e. on a field that is currently green and empty. Canada’s experience with greenfield FDI includes many examples where investment capital has led directly to building new and useful assets.

Examples include the Travers Solar Project in Alberta, which produces about 465 megawatts of clean power and at peak construction employed around 800 people; Roquette’s investment in the world’s largest pea protein plant in Manitoba; Sanofi’s investment in a new vaccine manufacturing facility in Ontario and LNG Canada, a liquified natural gas export facility in British Columbia that was made possible through the largest private sector investment in Canadian history by a consortium of five multinational firms from different countries.

It’s clear how building a new asset can bring additional capital, create jobs and contribute to growth. The example of LNG Canada, which is enabling export to Asian markets, also demonstrates the potential of greenfield FDI to increase market access, while Roquette’s state-of-the-art pea protein plant is expected to reshore pea processing, shifting some processing from India and China to Canada. By using cutting-edge technologies, investments like these can also lead to innovation-driven productivity enhancements while enabling Canadian workers to develop transferable skills related to advanced technologies.

Greenfield FDI is not without its complexities. It is worth noting that, in a competitive global environment, governments often seek to attract greenfield FDI through some combination of subsidies and tax breaks. Public investment can be used to attract investment to projects that align with broader policy priorities beyond jobs and growth, like Canada’s net-zero goals. Increases in FDI inflows to Canada in recent years have been largely attributed to government subsidies focused on clean energy and electric vehicle value chains–although the latter, in particular, have attracted criticism, as have the significant subsidies that made LNG Canada possible. In other cases, incentives used to woo multinational tech companies to set up offices in Canada have been criticized for attracting talent away from Canadian-owned firms and facilitating the transfer of IP out of Canada. In the most problematic instances, tax breaks, in particular, can attract a version of greenfield FDI that does not yield the looked-for benefits (as has been true in Ireland). These deals can be tricky to get right. If they are well designed, however, their alignment with policy priorities can enhance their public value.

It is also possible that greenfield FDI could in some cases displace domestic firms or capital that could have achieved similar or even bigger impact with appropriate public support. This counterfactual is particularly important to consider in areas that are vital to Canada’s economic sovereignty. For example, Canada’s critical minerals strategy makes clear the intent to prioritize domestic ownership across the value chain, from exploration and extraction to downstream product manufacturing and recycling, in partnership with Indigenous communities, in order to maximize the economic, social and environmental benefits to Canada – a goal that would be undermined if new projects were built and owned by foreign capital.

However, while each instance will have different trade-offs requiring careful consideration, in general, where greenfield FDI creates a new asset that would otherwise not have been built with domestic capital, claims of new jobs, growth, increased productivity and innovation and expanded market access are likely justified.

M&A FDI

Foreign acquisitions of Canadian firms present a very different picture, as the capital involved pays for very different things, and that drives different outcomes for jobs, for growth, productivity and innovation, and for market access.

Capital investment

In a typical M&A FDI deal, capital is used to pay existing shareholders. Unlike in greenfield investments, the capital is not used to build new assets in Canada. We’ve found this to be the most common misconception when discussing this topic, and it’s a critical one.

A common rejoinder to proposals to restrict FDI is to ask where the capital will come from, if not from foreign sources. While this may be valid in the case of greenfield FDI, this argument doesn’t make sense when applied to M&A. If an acquisition doesn’t happen, in most cases no replacement capital is required as the target Canadian company will simply continue to operate under Canadian ownership.

Further, the availability of investment capital will often be reduced by M&A FDI for two reasons. First, acquisitions are often funded with debt that will sit on the balance sheet of the acquired company, which may crowd out investment capital. For example, in the case of Parkland’s recent decision to sell to U.S.-based Sunoco, new debt of $2.65B USD will provide the capital required to pay shareholders. Second, the acquirer will often have operations in multiple countries, driving competition between jurisdictions to fund new projects.

Jobs

Acquisitions, foreign or domestic, are often predicated on “synergies” where jobs (usually high-paid head office, R&D or manufacturing jobs) are made redundant in the combined company as capacity is optimized and departments and functions are merged. These savings are how the acquiring company justifies paying a price high enough to get a deal done and will often occur at the acquired company.

This dynamic has been evident in Canada. AMD’s acquisition of ATI, the China National Offshore Oil Corporation’s (CNOOC) purchase of Nexen and U.S. Steel’s acquisition of Stelco all led to layoffs, the last of which resulted in a government lawsuit. The most recent example is the closure of Crown Royal’s blending and bottling facility in Amherstburg, Ontario, with those jobs moving to the U.S., causing Premier Doug Ford to pour out a bottle at a press conference as he lashed out at British owner Diageo. While each instance has its own context and explanations, these outcomes are not surprising as they are a common and often intentional outcome of M&A transactions.

Growth, productivity and innovation

Two of the most commonly cited advantages of FDI have to do with the expertise of multinational firms: increased productivity and transfer of the latest technology to the host country. But a recent German study looking at 25 years of German M&A FDI found no evidence of increased output (i.e. no growth) and revealed that almost all productivity gains were a result of reduced employment. It concluded that while technology transfer may be important in acquisitions in a less developed economy, it was not evident in Germany’s advanced economy. In economies where R&D and knowledge workers are more prevalent, like Canada, FDI may be more likely to seek to acquire new technologies and talent than to bring them to the country.

In statements about FDI’s productivity-enhancing benefits, the research cited rarely focuses on acquisitions, instead pointing to studies that find foreign-owned firms to be more productive than domestic ones, and implying that all FDI shares equally in this benefit. (In this Fraser Institute article, for example, only one of the studies cited to support these claims focuses on acquisitions, and the findings of this study are likely explained by the job losses described in the more recent German study). It is reasonable to assume that a greenfield investment in a new factory will use the latest technology and perhaps add competition to the market. While an acquisition could, in some cases, result in the foreign buyer upgrading facilities with cutting-edge technologies, this is unlikely to be a common occurrence and should not be assumed to be a benefit.

Canada’s experience is almost certainly similar to Germany’s. There are many examples of outward technology transfer. AMD’s acquisition of ATI was to acquire ATI’s technology, not to improve it. CNOOC’s acquisition of Nexen in 2013 was explicitly to transfer Nexen technical know-how to China. Alphabet recently acquired North and AdHawk in order to gain technology they didn’t previously have.

These acquisitions all represent the sale of Canadian technology and knowledge to other countries. They are detracting from, rather than contributing to, Canada’s innovation ecosystem and potential for future innovation-driven productivity and growth.

Access to markets

There is likely some validity to the claim that cross-border acquisitions can provide greater access to export markets for the acquired Canadian company. This could occur in cases where the acquiring company is well established in foreign markets and the acquired company is not, but produces a readily exportable product that is complementary to the acquiring company’s existing product line. In an ideal scenario, this could lead to an expansion of operations in Canada to service foreign market demand. This ideal scenario most definitely does not apply in all cases, however.

The winners in M&A FDI

Acquisitions, both foreign and domestic, have a long and well documented history of disappointing outcomes. But they are not without their winners. Aside from selling shareholders who are presumably getting a good price, senior executives at both firms stand to gain bonuses if they stay and golden parachutes if they leave. Executive pay also increases when companies get bigger through acquisition. Transactions are also very lucrative for the investment bankers and lawyers who manage the transaction and the accountants and consultants who help with integration.

To summarize, M&A FDI deals will benefit a relatively small number of people, whatever the outcome for the companies, workers and countries involved, but in most cases will not bring new investment capital into Canada, will often reduce Canadian employment, are unlikely to drive innovation-based productivity or growth and are often used to acquire Canadian technology, resources and expertise. There will be times when an acquisition will provide a benefit to Canada–for example, if the acquirer commits to a specific, near-term capital investment that was not already in the company’s plans or can improve access to global markets–but these are not typical.

Unless the acquiring company can prove otherwise, the base case for M&A FDI should be that it will not provide the benefits normally linked to FDI in commentary and textbooks.

The special case of technology start-ups

While M&A FDI deals involving Canadian tech start-ups typically fall well below the ICA thresholds for net benefit review by the government, it is worth noting that in these deals, the implications of preventing foreign acquisitions are harder to discern. On the one hand, tech startup founders and politicians have been complaining for years about how little advantage Canada gains from the IP it develops, with most of the benefit going to foreign companies through licensing deals and acquisitions (i.e. M&A FDI). On the other hand, funding for tech start-ups is very different from that of traditional businesses as these companies rarely generate cash or pay dividends, and access to venture capital often depends on the promise of a lucrative “exit,” when the company either lists on a public market or, far more likely, is acquired by a larger (often U.S.) competitor. There is a legitimate concern that if foreign companies were prevented from buying start-ups, access to venture capital in Canada would be far more constrained. We don’t have a clear answer to the question of how to balance these concerns, but others have written about how to facilitate paths to scale that don’t require foreign acquisition, and Ottawa is actively pursuing policies with this aim.

Why this matters now

When the Investment Canada Act (ICA) was enacted in 1985 by the Mulroney government, its objective was to encourage foreign investment, limiting reviews to larger transactions that could be “injurious to national security,” in place of the previous Foreign Investment Review Act (FIRA), which allowed for review of all FDI transactions and required a demonstration of significant benefit to Canada.

The ICA succeeded in ushering in an era of significant inward and outward investment, especially between the U.S. and Canada. While the Act has been strengthened several times, it has almost never been used to block acquisitions. However, forty years after its introduction, Canada faces a starkly different world, and the focus is shifting from encouraging investment to protecting Canadian economic sovereignty.

To that end, in March 2025, former Minister of Innovation, Science and Industry, François-Philippe Champagne, tightened ICA guidelines in response to direct threats from the U.S., the primary buyer of Canadian assets. It expanded its scope to protect against “the potential of the investment to undermine Canada’s economic security” in the face of “opportunistic or predatory investment behaviour by non-Canadians.”

There is no sign that the risks that drove the Minister to act are abating. The American administration is currently leaning on U.S.-owned companies to support its geopolitical objectives in relation to China. It would be naive to ignore the possibility that American owners of Canadian companies might be pressured to “undermine Canada’s economic security.” U.S. President Donald Trump has already signaled that he could use “economic force” to redraw the Canada-U.S. border or pursue annexation or simply to get the trade deal he wants. Just recently, Ontario’s Premier Doug Ford lashed out at the CEO of U.S.-based Cleveland-Cliffs, owner of Hamilton’s Stelco, for acting against the interests of their Canadian division and putting Canadian jobs at risk by pushing for higher American steel tariffs.

Canadian assets under U.S. ownership–for example, critical minerals mining operations, manufacturing plants and energy and electricity infrastructure–could be turned into bargaining chips, with implications for jobs, consumer prices, supply stability, domestic competition and future investment decisions.

In the face of these threats, FDI policy could be strengthened further, perhaps applying the standard set in 2024 for the critical minerals sector, where foreign investment is allowed only “in the most exceptional of circumstances,” to all M&A FDI. The threshold for net benefit review could also be lowered. Proponents of the rare acquisition deals that could be beneficial would still be able to make their case.

If more foreign acquisitions of Canadian companies are rejected, there will be some who argue this is a mistake, trotting out reasons Canada needs FDI that simply don’t apply to acquisitions. With Canada facing investment, employment and productivity challenges, the arguments to ignore geopolitical risks will be compelling. Understanding why these deals may in fact hinder investment, jobs and productivity will be critical in winning the argument in the public square.

One argument that will surely be used in favour of accepting foreign acquisitions is that actions Canada takes to reject deals could cause the rejected country to respond in kind. It is indeed likely that the U.S. – currently the main destination for outward FDI – would retaliate by restricting the ability of Canadian companies and investors, such as pension funds, to make investments in America. Economic sovereignty isn’t free, and this is a price we should arguably be willing to pay. Simply put, a dollar of investment by the U.S. into Canada yields a lot more control than a dollar of investment by Canada into the U.S. For example, while Sunoco’s purchase of Parkland would represent 15% of Canadian gas stations, a similar purchase by a Canadian company in the U.S. would represent less than 2% of those in America. While there might be some small sacrifice in returns for Canadian investors, in the current geopolitical environment, shifting investment to other countries or ideally to investing at home is a rational strategy.

Getting comfortable saying “no”

Many reports have been written about the pros and cons of FDI inflows in Canada. Despite that, both the fact that it is actually a poor barometer of economic health and the clear difference between greenfield and M&A FDI remain broadly misunderstood. Our objective here is to create a basic understanding of what FDI is and of when it is likely to be beneficial or harmful, and to provide language to those seeking to protect against cross-border acquisitions that could undermine Canada’s interests.

We know that FDI deals provide conflicting incentives for politicians. Rejecting transactions that are not in Canada’s best interest also reduces the total value of FDI. As long as FDI is seen as a barometer of economic health, politicians will be under pressure to ensure this number goes up, and to ignore the very different implications of different forms of FDI. But current threats to Canada’s economic sovereignty should override this tendency and we should expect to see some deals rejected. Ideally, this will lead to a shift in how FDI is described and analyzed, introducing long-absent nuance and sophistication to the public discourse and making it easier for politicians to analyze each new transaction on its merits.

This would be a good thing. For forty years, Canada’s default approach was to be “open for business,” which often led to the sale of important Canadian companies and assets, costing jobs and innovation capacity. Becoming comfortable saying “no” in the face of opposition from influential vested interests, and getting better at explaining the downside of acquisition FDI, will help both in the face of immediate geopolitical risk and in Canada’s long-term effort to build a more resilient economy.

The Canadian Tax Observatory announces Heather Scoffield as founding CEO

September 11, 2025, Ottawa (ON) – The Board of Directors of the new Canadian Tax Observatory (the Observatory) today announced the appointment of its founding CEO, Heather Scoffield. Her plans for the research and policy centre are ambitious.

“Heather Scoffield has been helping Canadians make sense of the economy for almost three decades,” said Matthew Mendelsohn, Chair of the Board. “It is sometimes hard for non-specialists to understand the nuances and implications of tax policy. I can’t think of any Canadian better placed than Heather to help Canadians make sense of the evidence and understand the implications of tax policy discussions on their own lives and on the ability of the country to meet the moment we face.”

Leading the Canadian Tax Observatory is a logical progression in Scoffield’s career, which has been devoted to driving a vigorous, informed national conversation on economic policy. Previously, she was Ottawa bureau chief at The Canadian Press, the economics columnist and Ottawa bureau chief at the Toronto Star, and most recently senior vice-president of strategy at the Business Council of Canada.

“Our current tax system is overly complicated – the product of so much history and politics over time, with so many unintended consequences, and with rules that are no longer responding to the realities of today’s economy,” said Scoffield. “I aim to drive in-depth research that pulls apart the strands of our current system so that we can thoroughly evaluate where we are and engage Canadians in a broad discussion about how to support economic growth while improving the fairness of Canada’s tax system.”

Over the next six months, the Observatory will connect with researchers in Canada, build alliances globally and develop its research agenda.

“Tax reform is in the air,” said Scoffield. “Before we attack the foundational issues inhibiting growth and fairness in Canada’s tax system, we need to ensure policymakers putting together this fall’s budget hear about the need for an equitable and efficient tax system in response to global uncertainty, tariff fallout and slow growth.”

The Observatory is funded through philanthropic donors, including major contributions from Social Capital Partners and the Euphrosine Foundation.

About the Canadian Tax Observatory

Established in 2025, the Canadian Tax Observatory is an independent non-profit devoted to helping people and policymakers understand the tax system. Through research, public education and collaboration, its goal is to advance a tax system that promotes economic growth, shared prosperity and tax fairness. The founding board of directors includes Chair Matthew Mendelsohn, CEO of Social Capital Partners, Niamh Leonard, Executive Director of Euphrosine Foundation and Jennifer Robson, Professor of Political Management at Carleton University. For more information, please sign up for the organization’s eNews, follow them on LinkedIn or visit them at www.canadiantaxobservatory.ca.

For more information, please contact:

Heather Scoffield, CEO

The Canadian Tax Observatory

heather@canadiantaxobservatory.ca

613-314-1198

Maple Ridge-based company now owned by its 750 employees | Maple Ridge-Pitt Meadows News

By Neil Corbett | This article first appeared in the Maple Ridge-Pitt Meadows News

A company based in Maple Ridge has made some business history, becoming the largest Employee Ownership Trust in Canada, and the first from the social services sector.

Taproot Community Support Services, which has 750 employees in B.C., Alberta, and a small number in Ontario, announced this week that an Employee Ownership Trust (EOT) acquired a majority share of the business. All employees have an equal shares in the company.

Taproot is the largest company to become EOT-owned since the federal government introduced this ownership model in 2024.

On an online call with the company CEO and the federal finance minister, Maple Ridge-based employee Kam Kaur offered her enthusiastic endorsement of the transaction.

“I’m really excited about being an owner. This is something to boast about, I’m going to boast about this with my friends,” she enthused.

She talked about how rare it is for a company to come under the ownership of its workers.

“This feels like you’re being valued,” Kaur added. “For me, this is the first thing I’m owning in Canada, so I’m really happy about it.”

CEO Mike Fotheringham said there is no financial risk for the employees. In fact, they will share in dividends. Last year, the company had a surplus of $1.6 million on $61 million in revenues, and he anticipates most employees will see dividends of approximately $1,000 to $1,500 per year, in addition to their wages.

“They keep a little extra money in their jeans, and share in our success,” he said.

He noted it’s a stable company, having been around about 42 years since it was founded in Maple Ridge.

“This is the next natural step in the evolution of our company,” said Fotheringham. “Becoming an EOT brings our inclusive values to life, makes all our employees true partners in our purpose-driven success, and ensures our company will remain locally grounded and Canadian-owned for the long term.”

The federal government voiced enthusiasm for the change.

“Taproot’s move to an Employee Ownership Trust is a game changer. It not only secures its future and empowers its team, but it also guarantees that the vital services children, youth and adults depend on will continue,” said the Finance Minister François-Philippe Champagne.

“This is a perfect example of what EOTs can do – they’re a powerful, timely tool that helps Canadian employees become owners of the businesses they work for, while helping entrepreneurs find the right people to carry their legacy forward,” he added.

Taproot provides support services to adults with diverse abilities, as well as vulnerable youth and families, supporting nearly 2,000 clients a year across 70 sites. They support clients in Maple Ridge, Langley, Surrey and across B.C. and Alberta. There are about 30 employees working in Maple Ridge.

Prior to the transition, Taproot was owned by a group of approximately 30 longtime and prior employees, some of whom were retired. Canada’s introduction of EOTs created a succession pathway that put the organization’s future into the hands of its workforce. Now every employee will have a stake in the business.

“We’ve worked hard, so it’s really nice to be rewarded for that, especially as frontline workers,” said Talica Bautarua, a community support worker at Taproot. “It feels like we’re in it together more now.”